Founded in 1883, Leggett & Platt (LEG) patented the first steel coil bedspring. The company has since become a diversified manufacturer of engineered components (innersprings, recliner mechanisms, adjustable beds, steel wire, seat frames, carpet cushion, armrests, etc.) used in bedding, furniture, carpet, automobiles, aircraft, and other products around the world.

Source: Leggett & Platt Investor Presentation

Source: Leggett & Platt Investor Presentation

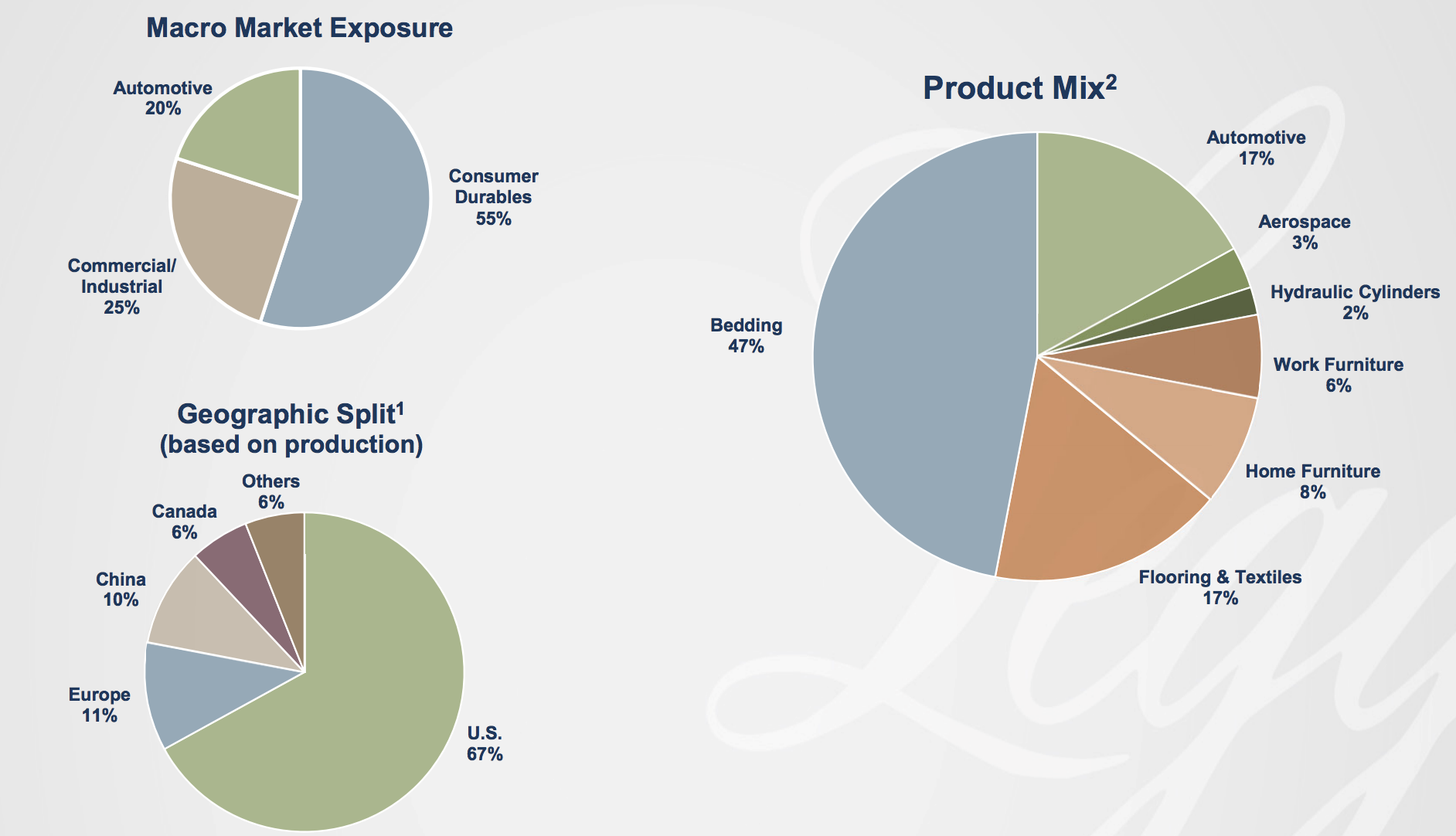

The majority of Leggett & Platt’s products serve the consumer durables market (primarily springs and foam used in bed mattresses). The company’s major customers include furniture makers, home improvement stores, and original equipment manufacturers (automotive and aircraft seats).

Most of the the firm’s sales are derived from the U.S. market (67% of revenue), but Leggett & Platt also has a presence in overseas markets, including fast-growing emerging economies such as China (10%).

Source: Leggett & Platt Investor Presentation

Source: Leggett & Platt Investor Presentation

Leggett & Platt is a dividend aristocrat and has increased its dividend for 48 consecutive years.

Business Analysis

Leggett & Platt’s impressive dividend growth track is fueled by the firm’s long-standing customer relationships (the company has been in the industry for over 100 years), economies of scale (the firm is also vertically integrated), focus on innovation, and global distribution system.

Leggett & Platt has built up a large portfolio of intellectual property over the years. For example, the firm has amassed more patents in bedding than anyone else, yet it only spends about $25 million per year on R&D, or less than 1% of revenue.

This low amount of spending is due to the fact that most of Leggett & Platt’s products have long life cycles, meaning the company doesn’t have to continuously redesign them and can amortize its costs better over time.

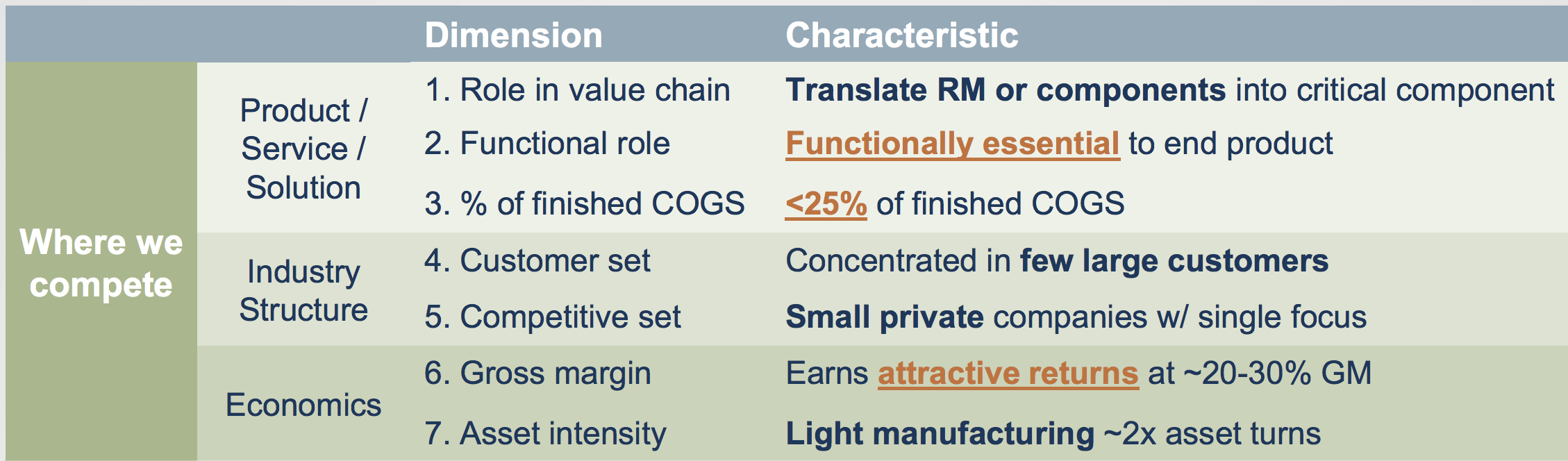

By focusing on components that are functionally essential to end products but typically represent less than 25% of a product’s finished cost, Leggett & Platt is also better positioned to price its products based on the value they provide rather than on the cost of its raw materials.

Source: Leggett & Platt Investor Presentation

Source: Leggett & Platt Investor Presentation

The niches Leggett & Platt competes in generally have a slow pace of change, too. While the processes and materials used to produce certain goods evolve over time (e.g. foam mattresses), the problems solved by mattresses and furniture are timeless.

About two thirds of bedding and furniture purchases are also made to replace existing products, making it more difficult for new entrants to quickly take market share or capitalize on emerging trends.

Leggett & Platt’s vertical integration helps ensure it is often one of the lowest cost providers of its products, too. For example, the firm owns a steel rod mill and machinery that produces much of the steel wire it uses.

The firm also benefits from having manufacturing facilities located around the world, allowing it to steer clear of tariff issues and source raw materials at the cheapest global rates.

Coupled with its entry into key markets many decades ago, Leggett & Platt has built No. 1 or No. 2 market share positions in most of its categories. The company has also extended the scope of its business with the help of acquisitions.

In 1960, bedding components represented nearly 100% of Leggett’s sales. Bedding represents less than half of the company’s revenue today, underscoring the firm’s expansion into adjacent markets over the last 50-plus years.

Acquisitions have helped the company stay relevant in its existing markets as well. For example, in 2018 Leggett & Platt acquired Elite Comfort Systems (ECS) for $1.25 billion. ECS is a leader in high-quality specialty foam used in bedding and furniture markets.

Premium foam and hybrid mattresses are expected to gain share as online mattress sales continue growing rapidly. “Boxed bedding” is an emerging trend, especially in the online mattress channel, and ECS derived 30% of its revenue from these products, improving Leggett & Platt’s long-term positioning.

Thanks to its adaptability and competitive advantages, Leggett & Platt has excellent profitability. In fact, the company’s operating cash flow has exceeded capital expenditures and dividends every year for 30 years.

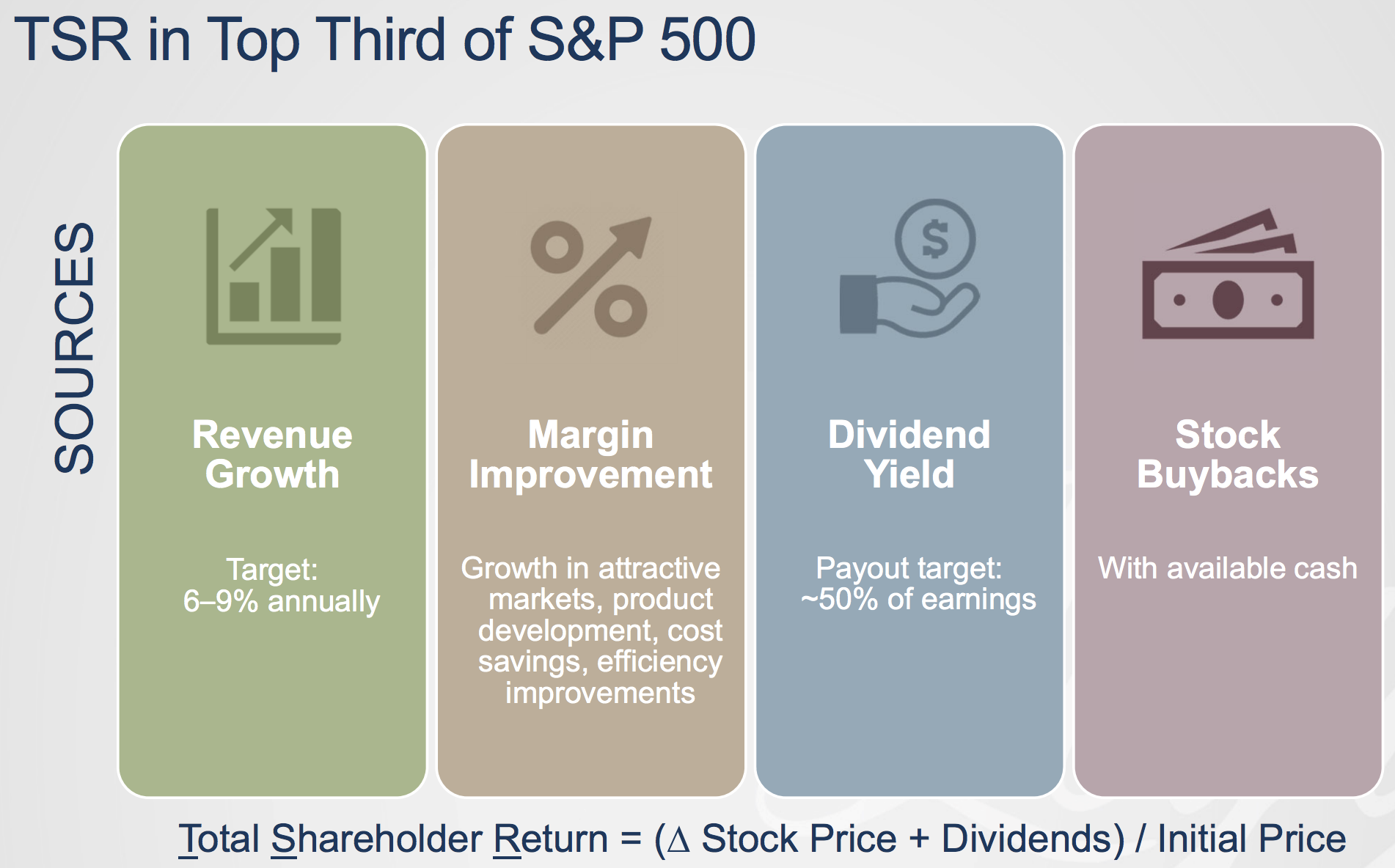

Going forward, management expects the business to continue generating 6% to 9% annual revenue growth in the long term, including about a 2% contribution from acquisitions.

Expanding its addressable markets in bedding (compressed mattresses, online sales, etc.) and automotive (cables, electronics, actuators, etc.) are key growth drivers, along with developing new growth platforms in markets such as aerospace and hydraulic cylinders.

Margins are also expected to tick higher, and a 50% payout ratio target should ensure the dividend remains well covered.

Source: Leggett & Platt Investor Presentation

Source: Leggett & Platt Investor Presentation

Overall, the company’s long-term goal is to achieve total returns in the top third of S&P 500 companies, and management has historically proven that it has the disciplined capital allocation skills to usually hit its growth targets.

However, there are several risks investors need to be aware of that could cause Leggett & Platt to miss its ambitious growth and total return targets.

Key Risks

In the short term, Leggett & Platt’s business is sensitive to several macroeconomic factors that are beyond its control. Changes in raw material costs (especially steel), foreign currency exchange rates, and consumer spending trends (bedding, furniture, cars) have materially impacted the company’s quarterly sales and earnings in the past.

While these will remain important factors going forward, they seem unlikely to affect Leggett & Platt’s long-term earning power.

The bigger issue to monitor is Leggett & Platt’s ability to continue delivering profitable growth as it manages changes across the numerous product lines it competes in.

For example, bedding accounts for about half of Leggett & Platt’s total revenue and is undergoing meaningful change. Over the next five years management expects the direct-to-consumer channel (i.e. online bed-in-a-box brands) to grow to roughly 40% of the market and private label retail to reach about 25%.

This could put pressure on some of the mattress stores Leggett & Platt works with, and the company is also adapting to the rise of hybrid mattresses, which are more complex to make since they use memory foam and innersprings.

Leggett & Platt is trying to stay ahead of these changes and others with investments in innovation and acquisitions of businesses like ECS. However, with so many different products to oversee, it could be difficult for management to get the company firing on all cylinders and fend off new competitors.

After all, not every niche will prove to be profitable in the long term. In fact, Leggett & Platt has pared back its number of business units from nearly 30 to less than 15 today as management moved away from commoditized (i.e. low margin) sales and placed greater emphasis on specialized products.

Going forward, investors must trust in management’s portfolio management capabilities, which includes acquisitions. Buying ECS added significant debt to the balance sheet, reducing some financial flexibility to make other acquisitions over the next couple of years.

Should Leggett & Platt pursue another large deal in the future and overpay or miss on its expected synergy benefits, then investors could lose some of their faith in management and the firm’s ability to hit its growth targets. For now, the company deserves the benefit of the doubt due to its solid track record.

Closing Thoughts on Leggett & Platt

Leggett & Platt is an impressive industrial company that few investors have heard of. Management’s disciplined and conservative growth strategies, combined with the firm’s strong balance sheet and conservative capital allocation, have resulted in consistent profitability and nearly 50 years of uninterrupted dividend growth.

While Leggett & Platt’s track record of adapting to changing conditions and paying steadily rising dividends is appealing, investors should remember that the best time to buy a stock like this is usually during a short-lived cyclical downturn in its end markets.

— Brian Bollinger

Sponsored Link: Simply Safe Dividends provides a monthly newsletter and a comprehensive, easy-to-use suite of online research tools to help dividend investors increase current income, make better investment decisions, and avoid risk. Whether you are looking to find safe dividend stocks for retirement, track your dividend portfolio’s income, or receive guidance on potential stocks to buy, Simply Safe Dividends has you covered. Our service is rooted in integrity and filled with objective analysis. We are your one-stop shop for safe dividend investing. Brian Bollinger, CPA, runs Simply Safe Dividends and previously worked as an equity research analyst at a multibillion-dollar investment firm. Check us out today, with your free 10-day trial (no credit card required).

Source: Simply Safe Dividends