Real estate investment trusts (REITs) have momentum now. And don’t let their terrific 2019 scare you—next year is setting up to be even better thanks to Jay Powell’s gang of doves!

I’ll reveal three strong REITs for 2020 at the end of this article. Together they give you growing dividends that double (and even triple) the market’s payout. And to be honest, one isn’t exactly a REIT—it’s a REIT-owning closed-end fund (CEF) that drops a huge 6.5% dividend into your account every month.

REITs: The Ultimate Rate-Proof Play

First, no matter what Jay Powell says, you can take this to the bank: more rate cuts are on the table as the on-again, off-again trade war lingers and the president batters the poor fellow tweet by tweet.

That’s why I’m betting on another “Powell pivot” toward rate cuts in 2020, just like we saw in January. I’m sure I don’t have to tell you what that did for REITs:

Powell’s Flip-Flop Ignites REITs

But what if I’m wrong and rates take a surprise jump next year?

But what if I’m wrong and rates take a surprise jump next year?

Good news: REITs will be just fine, because rising rates go hand in hand with economic growth (the side of the story everyone ignores), which drives up REITs’ occupancy and rents.

But rising rates do tend to separate the stars from the duds in REIT-land, so you’ll want to snap up trusts with high—and rising—payouts (as dividend growth is a key share-price driver).

No matter what happens with rates, you’ll need your payout locked in by rising funds from operations (FFO, the REIT equivalent of earnings per share) and a safe payout ratio (because of REITs’ steady cash flows, “safe” is usually anything below 90%).

Better still if your REIT is riding a megatrend like, say, aging baby boomers.

We Bagged 109% Gains From This REIT as Rates Rose

A good example? Medical Properties Trust (MPW), which I recommended in Contrarian Income Report in late 2015, in the run-up to the Fed’s first hike since before the Great Recession.

MPW ticked all my boxes, starting with its niche as the only publicly traded firm investing solely in licensed hospital facilities (of which folks 65 and up are the biggest users). Back then, MPW was pumping out cash: FFO had soared 82% in the preceding five years.

That was showing up in the dividend—the payout edged up 5% in each of the preceding two years. And bear in mind this payout was already starting from a high bar, with a mammoth 7.6% yield!

What happened?

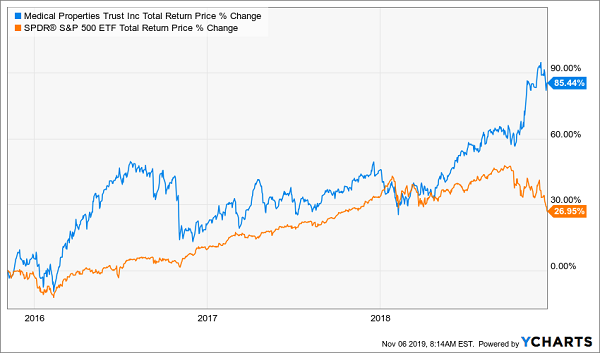

As rates headed higher, MPW crushed the market. In fact, by the time the Fed said it would stop raising rates in December 2018, MPW had tripled the S&P 500’s return!

Rates Rise, MPW Soars

We held on as this “rate-proof” REIT kept soaring, even after Powell’s January pivot. But by March 2019, with our total return hitting 109% and MPW’s dividend whittled down to 6.1%, it was time to check out.

We held on as this “rate-proof” REIT kept soaring, even after Powell’s January pivot. But by March 2019, with our total return hitting 109% and MPW’s dividend whittled down to 6.1%, it was time to check out.

MPW is a great example of how a well-chosen REIT can hand you big gains (and dividends) no matter what rates do—which brings me to the three real estate plays I have for you today.

Rate-Proof REIT No. 1: National Health Investors (NHI)

NHI picks up where MPW left off: it’s a 5.2%-yielder that also invests in medical facilities, but it focuses on seniors’ housing and skilled-nursing facilities, rather than hospitals, making it an even better play on our aging population.

NHI drops cash into these properties and nails down strong returns on its money. One way it does so is through sale-and-leaseback deals (where owners sell their facilities to NHI, then lease them back, giving the REIT—and us—steady income).

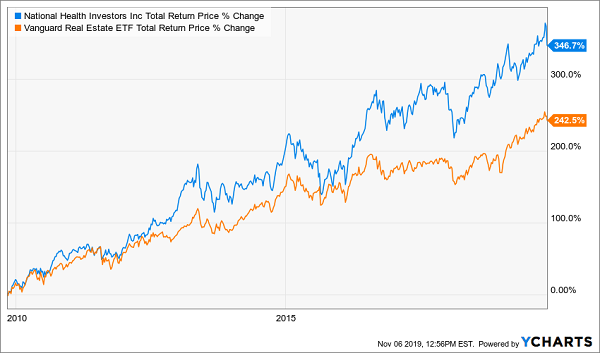

The result? NHI crushed the average REIT in the last decade, with much of that gain in cash, thanks to its high payout and 62% dividend growth:

NHI Rides Its Dividend to 347% Returns

A big benefit of healthcare REITs—including NHI—is that they dial back your portfolio’s volatility.

A big benefit of healthcare REITs—including NHI—is that they dial back your portfolio’s volatility.

Here’s what I mean: NHI’s beta rating is 0.27, making the stock 73% less volatile than the market. This also means the REIT can (and does) rise in a meltdown, which is exactly what happened at the end of 2018:

Market Collapses—NHI Owners Profit

Finally, NHI’s payout ratio, at 83% of the midpoint of forecast 2019 FFO, means the dividend is safe and has room for further growth.

Finally, NHI’s payout ratio, at 83% of the midpoint of forecast 2019 FFO, means the dividend is safe and has room for further growth.

Rate-Proof REIT No. 2: National Retail Properties (NNN)

National Retail Properties, payer of a 3.7% dividend, has a setup almost as slick as MPW’s: it owns outdoor malls whose tenants rent under a “triple-net-lease” model, where they pay all the bills: maintenance, insurance, and utilities.

NNN? It simply collects the checks!

Tenants include 7-Eleven, Mister Car Wash, Camping World, LA Fitness and AMC Theaters (AMC), as well as restaurant chains like Chuck E. Cheese and Frisch’s. I think you’ll agree that this isn’t exactly a lineup of Amazon.com (AMZN) victims.

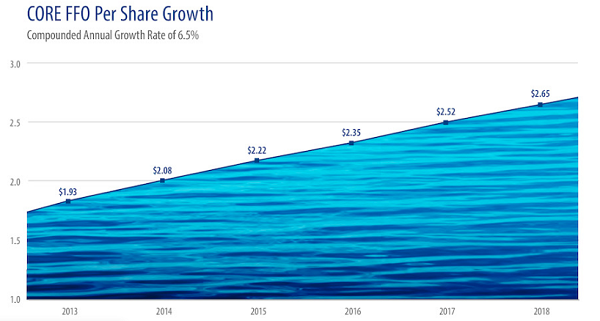

As you can imagine, triple-net leases lead to smoother FFO growth, because they pass off many big, unpredictable expenses to the tenant. That’s exactly what we’ve seen with NNN:

Source: National Retail Properties 2018 annual report

Source: National Retail Properties 2018 annual report

The REIT just raised its guidance and now sees 2020 FFO of $2.79 to $2.82 a share. That estimate easily supports the dividend—which yields 3.7% and is just 73% of the forecast’s midpoint. That FFO growth also sets the table for higher dividends, on top of the 23% payout increase investors have enjoyed in the last five years.

Rate-Proof REIT No. 3: Cohen & Steers Quality Income Realty Fund (RQI)

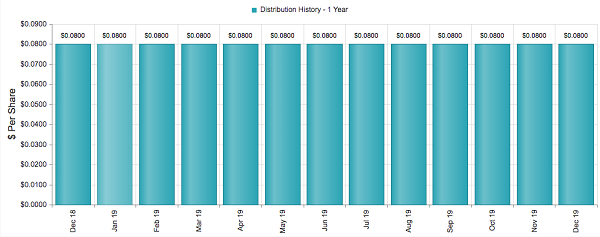

Finally, we’re going to boost our yield a bit higher with RQI, the CEF I mentioned off the top—it pays an outsized 6.5% payout every month:

RQI’s Dividend Matches Your Monthly Bills

Source: CEF Connect

Source: CEF Connect

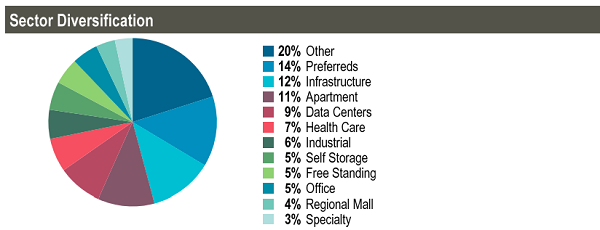

I usually prefer buying REITs individually, so I can focus on sectors with strong prospects, like healthcare. But I’ll make an exception for RQI, which diversifies across the REIT space and gives you some exposure to preferred shares, another high-yield vehicle too many people ignore.

In fact, RQI’s sector weighting lines up almost exactly with the REIT sectors I see performing best next year:

Source: Cohen & Steers Quality Income Realty Fund fact sheet

Source: Cohen & Steers Quality Income Realty Fund fact sheet

There is one caveat here: RQI trades at a 0.54% premium to its net asset value (or slightly more than the value of its portfolio holdings). But that’s worth paying for this management team, which has nailed down the top return, based on market price, of any US-focused REIT CEF since launch at 10.4% annualized.

— Brett Owens

This Is PROVEN to Boost Your Income 4X—Instantly [sponsor]

If you’re hunting for safe, steady, 10%+ yearly returns, I’ve got the solution: my just-released “Perfect Income Portfolio.” I’ll give you all the details right here.

I know the word “perfect” might sound just a little outlandish, but what I’m about to show you is my life’s work. I’ve calibrated this proven system over years of testing and analyzing to do one thing: hand you a reliable 10%+ return in good markets and bad.

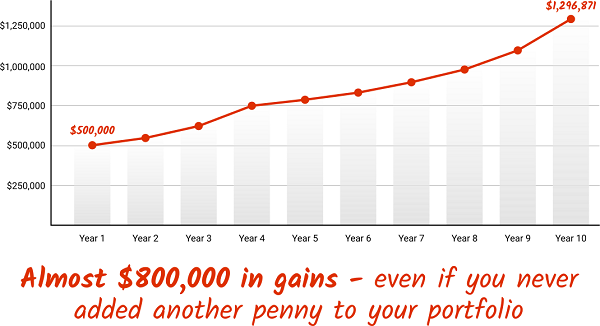

I’ve got the proof: here’s what would have happened to your money if you’d followed this powerful strategy over the last decade:

What’s more, this stout collection of investments hands you most of your return in safe dividend cash!

What’s more, this stout collection of investments hands you most of your return in safe dividend cash!

In fact, if you’re stuck “grinding it out” on the paltry dividends the S&P 500 pays, this portfolio is the answer: I’m confident it will let you double, triple—even quadruple—your income stream.

Think about that—drop $500K into this portfolio and, a year later, you could be sitting on $50,000 in dividends and gains!

A Steady 10%+ Return—Year in and Year Out—Made Easy

I’ve devised this portfolio to be dead simple to set up—it consists of just 3 often-ignored investment vehicles (and yes, REITs are one of them).

When you read my full report here (it’ll take you 10 minutes, tops), I’ll walk you through each of these three corners of the market and make sure you have the names and tickers you need to set up your own Perfect Income Portfolio today.

I could charge thousands for insider access to this portfolio, but I’m giving you the keys to the kingdom right now.

Don’t miss out. Discover my full Perfect Income Portfolio for yourself and learn how to 2X, 3X and even 4X your income starting today.

Source: Contrarian Outlook