“Brett, give me some bond funds with big yields. And it’d be great if their prices never went down!”

My money manager friend was chasing the holy grail of retirement income. He wanted safe payouts from bonds to balance his clients’ stock exposure.

“How about the Artisan High Income Investor Fund (ARTFX)?” I replied. “It pays a steady 6% or so. And it never goes down.”

Up, Up, Up With Barely a Blip

“The only problem is that it doesn’t quite have double-digit yearly return potential. And that’s prevented me from recommending it to my Contrarian Income Report subscribers.”

“The only problem is that it doesn’t quite have double-digit yearly return potential. And that’s prevented me from recommending it to my Contrarian Income Report subscribers.”

Our CIR portfolio has returned 11.7% per year since inception.

Adding ARTFX to the mix would drag our retirement boat lower!

I prefer price upside alongside my dividends.

And for big gains we must consider closed-end funds (CEFs), which are bought and sold with less efficiency than blue-chip stocks and ETFs.

The dividend dictionary is filled with the latter.

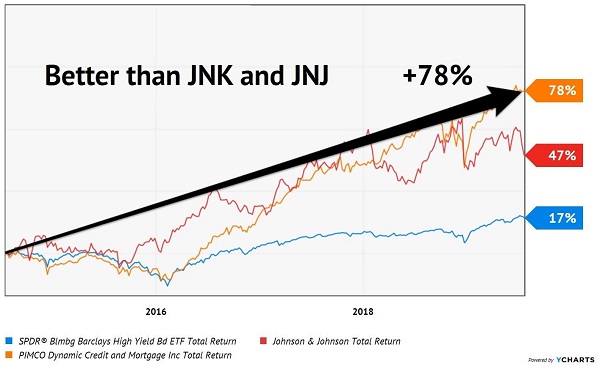

We know Johnson & Johnson (JNJ) for its century-old dividend and the SPDR Bloomberg Barclays High Yield Bond ETF (JNK) because its ticker spells “junk.” But few turn the page to the underrated PIMCO’s Dynamic Credit and Mortgage Fund (PCI).

This is a shame because PCI pays a generous 8.3% today while JNJ yields just 3% and JNK pays 5.6%. It’s doubly ironic because PCI has more than doubled the returns of its two better-known “competitors”:

PCI Pays More, Goes Up Faster Than JNJ and JNK

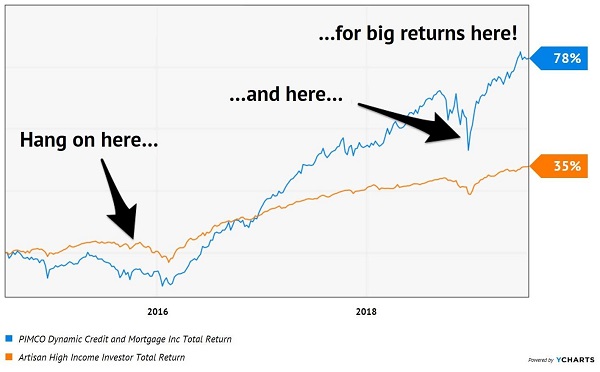

PCI’s payout is safe but its price is subject to market whims. As a CEF, the fund has a fixed amount of shares (like an individual stock). This means its price can swing up and down (like an individual stock). Over the long haul this “volatility” works in our favor as patient investors, but it can cause indigestion for folks who watch their tickers daily (or worse, hourly!)

PCI’s payout is safe but its price is subject to market whims. As a CEF, the fund has a fixed amount of shares (like an individual stock). This means its price can swing up and down (like an individual stock). Over the long haul this “volatility” works in our favor as patient investors, but it can cause indigestion for folks who watch their tickers daily (or worse, hourly!)

The Hare Won (As Long As You Didn’t Sell)

And I get it–some of you just do check your stock quotes every day, and that’s just how it’s always going to be. Or you may have plenty of potential action packed into the rest of the portfolio (whether it’s dividend growth or cryptocurrencies or weed stocks… I’m not judging) and you just want anchors that can help steady the ship and pay you every month no matter what happens.

And I get it–some of you just do check your stock quotes every day, and that’s just how it’s always going to be. Or you may have plenty of potential action packed into the rest of the portfolio (whether it’s dividend growth or cryptocurrencies or weed stocks… I’m not judging) and you just want anchors that can help steady the ship and pay you every month no matter what happens.

A bond CEF is a great addition to a “no withdrawal” portfolio, or an account in which you are comfortable letting prices do what they will while you collect your monthly and quarterly payouts. But bond CEF prices are going to fluctuate day-to-day, while ARTFX is a distribution rock.

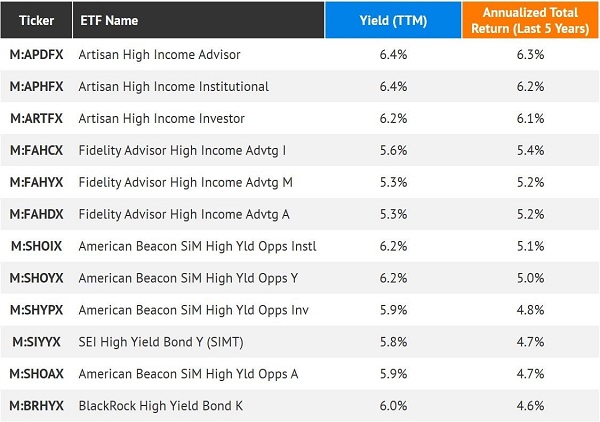

Want more bond rocks? Let’s dig. Here are 11 more funds that, like ARTFX, meet the following strict criteria.

First, they pay 5% or better. While we’re not looking for moonshots, we are looking for meaningful yield.

Second, they’ve returned 4.5% or better annualized over the last five years. This means these funds have at least “returned their yields.” They’re not tapping their own portfolios (or net asset values, NAVs) to pay us.

And finally, their “betas” are in the basement at 0.2 or below. This is the measure of how much the stock swings relative to the broader market. If the S&P 500 moved 10 points, we’d expect these prices to only move a point or two at most.

The 12 Safest Bond Mutual Funds That Actually Pay

The 12 funds above are all mutual funds, a tribute to the value that an active manager can add in Bondland. Now I know that some investors prefer ETFs, either by choice or by necessity. This is doable but we must widen our strike zone a bit to allow for lower yields and yearly returns:

The 12 funds above are all mutual funds, a tribute to the value that an active manager can add in Bondland. Now I know that some investors prefer ETFs, either by choice or by necessity. This is doable but we must widen our strike zone a bit to allow for lower yields and yearly returns:

The 8 Safest Bond ETFs That Actually Pay

As we discussed with ARTFX, I don’t anticipate I’ll ever formally recommend one of these funds in CIR. Their total returns are unlikely to clear my high-single-digit yearly hurdle. However, they are good ideas for anyone looking to tie down their portfolio during any market turbulence. These 5% and 6% yields are about as steady as they come.

As we discussed with ARTFX, I don’t anticipate I’ll ever formally recommend one of these funds in CIR. Their total returns are unlikely to clear my high-single-digit yearly hurdle. However, they are good ideas for anyone looking to tie down their portfolio during any market turbulence. These 5% and 6% yields are about as steady as they come.

The Best Bond Funds: CEFs for 8.5% Yields and 78% Returns

I prefer CEFs to mutual funds and ETFs because:

- They yield more, and

- They can go up in price more quickly.

In fact, CEFs flash a crystal-clear buy signal when a big price rise is coming. You’ll find it in the discount to NAV, which is the percentage by which the fund’s market price trails the market value of all the assets in its portfolio (known as the net asset value, or NAV).

This makes our plan simple: wait for the discount to sink below its normal level and make our move. Then we’ll keep rolling our dividend cash into that fund until its discount closes (or swings to a premium).

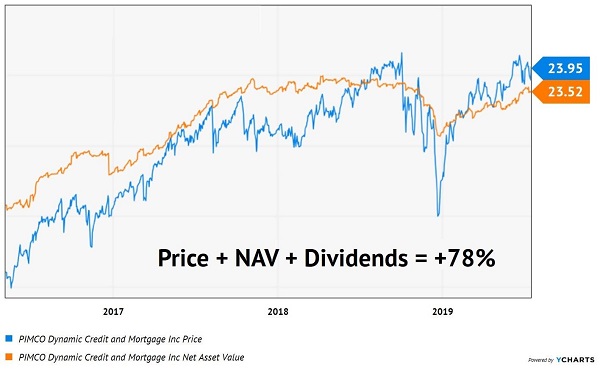

This is exactly what happened when we bought the PIMCO Dynamic Credit and Mortgage Fund (PCI) in my Contrarian Income Report service in May 2016. Not only did we collect the fund’s generous dividend, but we won two more ways over the three years we’ve held PCI because its:

- NAV increased (orange line below), and …

- Its discount window tightened as its price (blue line) caught up with—and eventually surpassed—its NAV.

2 Ways to Win for 78% Total Returns

We’ve earned 78% total returns from PCI, thanks to the dividends we’ve collected, the NAV gains we’ve enjoyed and the discount window closing entirely—and flipping to a premium!

We’ve earned 78% total returns from PCI, thanks to the dividends we’ve collected, the NAV gains we’ve enjoyed and the discount window closing entirely—and flipping to a premium!

For much of PCI’s run, I’ve had a “buy” rating on the fund when this “twofer” potential remained in place, making it a perfect destination for both reinvested dividends and new cash my members had available to invest.

For a period of time, though, PCI has cruised along as a “hold” for us. This happened after its price rallied so furiously that its discount window closed.

When this happens, it makes sense to bank our PCI dividends (or “redirect” them to our other Contrarian Income Report buys) and wait for our next buying opportunity.

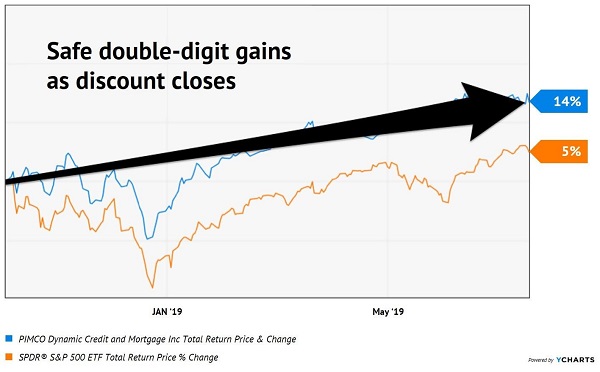

That’s what happened with PCI. Its discount window opened again in the late 2018 selloff — on October 5, to be precise — when its market price fell below my $23.50 buy-up-to level. Investors who got in then picked up a nice 14% total return, nearly three times the market’s gain!

Buy Window Opens, Gains (and Dividends) Ensue

As you can see in the orange line above, your typical S&P 500 investor didn’t come anywhere close to those returns in that time.

As you can see in the orange line above, your typical S&P 500 investor didn’t come anywhere close to those returns in that time.

— Brett Owens

Yours Now: My Next 8%+ (Monthly) Income Buys [sponsor]

As you can probably guess from the chart above, PCI is trading at a massive premium to NAV now, so I’ve switched it back to a hold.

But it’s only a matter of time before our buy window slides open again—and we can put more cash into this amazing 8.7%-yielder.

When you take a no-risk trial to Contrarian Income Report—full details on that and my complete monthly-dividend strategy here—you’ll be the first to know when the time is right.

Meantime, if you’re looking for some stout monthly high yielders to buy NOW, fear not! I’ve got you covered there, too.

Those would be the stocks, high-yield REITs and CEFs in my powerful “8% Monthly Payer Portfolio.” With just $500K invested, this dynamic collection of investments will hand you a rock-solid $40,000-a-year income stream. That’s easily enough for most folks to retire on.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it. Thanks to this breakthrough portfolio’s reliable monthly dividends, you can look forward to the steady drip of $3,333 in income, month in and month out—on your $500K, give or take a couple hundred bucks!

Full details on these stalwart income plays are waiting for you right here. You’ll discover:

- An 8.1% payer that’s set to rake in huge profits from an artificially depressed sector.

- The brainchild of one of the top fund managers on the planet that’s giving out a generous 9.1% yield.

- And a rock-steady 6.9% dividend trading at a massive discount to NAV.

Don’t miss your chance to start tapping this retirement-changing dividend stream while you can still get in at a bargain. Click here to get full details on every stock in my “8% Monthly Dividend Portfolio”: names, ticker, symbols, buy-up-to prices—everything you need to know to buy with confidence.

Source: Contrarian Outlook