Forget today’s pathetic Treasury rates. And forget the lousy payout on your typical S&P 500 name, too.

Put your nest egg in either and you’re locking in an income stream that’s actually less than zero for years to come!

I know that sounds crazy—I’ll get into precisely what I mean, and how it could jeopardize your golden years—shortly.

Then I’ll show you my two-step dividend strategy (and four specific stocks and funds you can buy now).

Put all four of these picks together and you’ve got a perfect setup for these days of miserly yields, giving you gaudy 6.1%+ payouts today and an incredible 20%+ cash stream in short order!

How Powell Crushed Savers

First, if you’re disappointed in the dividend options out there today, you can blame one man: Jay Powell. (Actually, you’ll have to get in line to dump your frustrations on the poor fellow’s head!)

We all know that Powell’s clumsy “pivot” from rate hikes to rate cuts at the start of 2019 sent stocks soaring (and dividend yields plunging—as you calculate yield by dividing a company’s annual dividend payout into is current share price). Powell’s lurch also sent the yield on the 10-year Treasury note (in orange below) crashing.

Powell’s Mr. Bean Act Leaves Yields Cold

And now we’re staring down the boogeyman of negative interest rates.

Think it can’t happen? There’s already $16 trillion in debt sloshing around the world yielding less than zero.

Yields could have a minus sign in front of them in America next, especially if an economic pullback sends the Federal Reserve on a stimulative turn. Former Fed Chair Alan Greenspan recently said: “You’re seeing [negative] rates pretty much throughout the world. It’s only a matter of time before they’re in the United States.”

Imagine buying a Treasury note now and, 10 years on, getting back less than you put in! It’s a recipe for retirement poverty. And it’s made the “dividend two-step” I’ll show you now even more urgent.

Let’s start with …

Step 1: Get Cheap 8%+ Dividends Here

True, there are few cheap dividends in the S&P 500 these days. But I say “who cares!” Because there are still plenty to be had in other, less-traveled corners of the market.

Consider one of my favorite vehicles: closed-end funds (CEFs). They’re the antidote to lousy yields: my Contrarian Income Report service, for example, holds nine CEFs yielding 7% on average (not including the fact that the payouts on our municipal-bond CEFs are tax-free for most Americans).

The highest payer? It’s throwing off a gaudy 9% payout—which it delivers every month—as I write this.

Here’s where the bargains come in: unlike other types of funds, CEFs’ share counts are mostly fixed after their IPOs. As a result, investors can bid their shares totally out of whack with the value of the fund’s portfolio—otherwise known as its net asset value, or NAV.

The upshot? We only buy when CEFs are trading at a discount to NAV. We’ll collect our big dividends while these “discount windows” slam shut, propelling our shares higher.

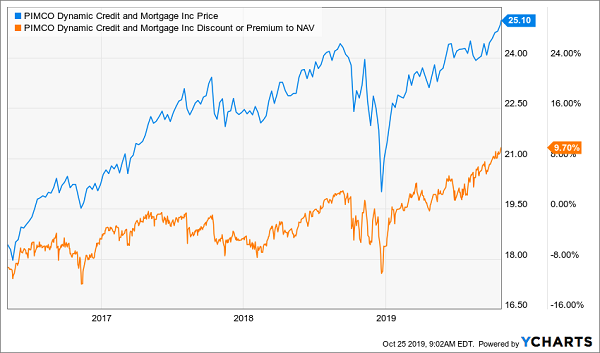

You can see this in action with the PIMCO Dynamic Credit and Mortgage Fund (PCI), which I recommended in Contrarian Income Report on May 6, 2016, when it traded at a 9.3% discount. Since then, PCI’s discount has flipped to a 9.7% premium.

That’s right! Investors are currently willing to pay $1.10 for every $1 of the fund’s assets.

And every time the fund’s discount has shrunk along the way, it’s pulled PCI’s market price up with it:

PCI’s Shrinking Discount Yanks Its Price Up

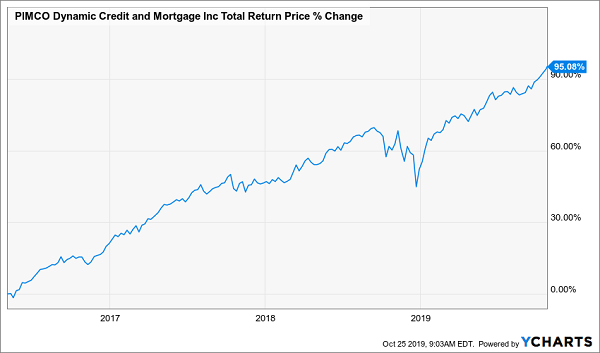

And if you throw in PCI’s outsized dividend (an 8.4% yield currently, paid out every month), the 36% price gain above transforms into an incredible 95% total return—with most of that in safe dividend cash.

Dividends Boost PCI’s Return 2.6X

But with PCI now boasting a premium, I no longer recommend it for new money (though its 8.3% yield makes it a great fund to hang on to if you already own it).

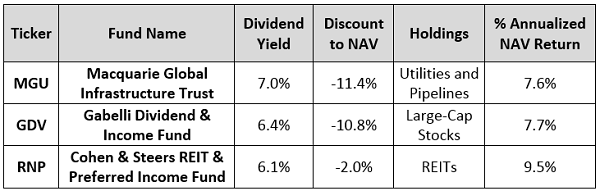

If you’re hunting for cheap CEFs to buy now, here are three that are more than worthy of your attention. All of them tick three boxes I insist on before buying a CEF:

- A 6% + dividend yield

- A discount to NAV

- 7%+ annualized returns on NAV since inception.

3 More Bargain CEFs You Can Buy Now (Ranked by Discount)

Now let’s move on to our next strategy for “Powell-Proofing” your portfolio. It’s an “automatic” dividend machine that’s even simpler than buying CEFs!

Step 2: “Stair-Step” Your Way to a Safe 20.3% Yield

In fact, there’s really only one step here: buy dividend growers. But not just any dividend growers—if we want to pump up our yield fast, we need payouts that are accelerating.

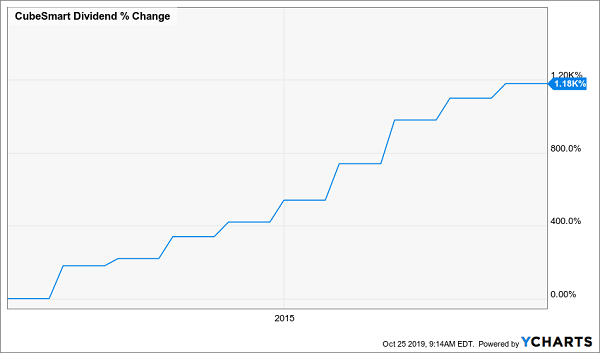

You can see this in action with CubeSmart (CUBE), a REIT in the self-storage space—a business so boring it would make even the most conservative investor sleepy. But the company’s dividend story is anything but!

CUBE pays a 3.7% dividend. That’s okay—double what the typical stock pays. But check out the incredible 1,180% payout growth CUBE delivered in the last decade:

1,180% Payout Drives a 20.3% Dividend

In other words, if you’d bought then, you’d be yielding 20.3% on your buy today!

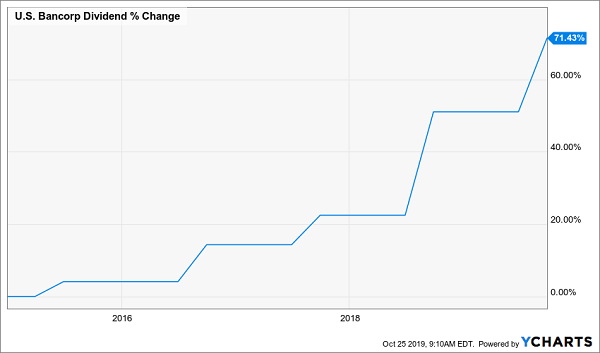

However, as you can see above, CUBE’s payout growth is now petering out. That’s not the case with US Bancorp (USB). Check out how the firm’s dividend has taken off—jumping 71% in the last five years—and is accelerating:

USB’s Dividend Takes Flight

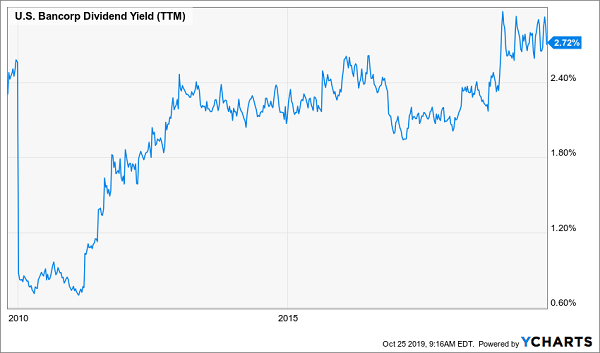

Funny thing is, investors haven’t (yet) taken notice and bid up the share price at nearly the same rate as the payout has risen. (It’s common for shareholders to take a while to notice a sprouting payout, and that delay is usually a great time to buy.)

In USB’s case, this lag has given us the chance to start our “automatic” dividend machine with a yield that’s very close to a 10-year high:

Investors Miss the Memo on USB’s Payout Growth

But how do we know USB’s dividend will keep accelerating? For one, the bank only pays out 30.5% of cash flow as dividends as I write this, well below my “safety margin” of 50%. Meantime, USB is overcoming lower interest rates through loan growth, helping power earnings per share higher (up 8.5% in the third quarter).

The kicker? Rate-driven pessimism around all banks has given you a chance to buy USB at 11.5-times free cash flow. So if you’re looking to fill out your finance holdings, now would be a good time to pick up USB.

— Brett Owens

A New (and Easy) Way to Get Paid $40,000 a Year Forever [sponsor]

This strategy—which delivers high yields now and dividend growth to boost your nest egg (and dividends) down the road—is how every investor should approach retirement.

Problem is, most folks have no idea how to find the high safe dividends (and fast payout growth) they need to make it happen. That’s exactly why I wrote the article you just read. And now I’m going to go further and give you my new “8% Monthly Dividend Portfolio.”

This sturdy collection of investments gives you the best of both worlds: big cash payouts now, steady growth in your income stream and one other thing investors tell me they want all the time:

Dividends paid out monthly, so they match up perfectly with their bills!

This unique portfolio comes to you fully stocked with high-yielding stocks, real estate investment trusts (REITs) and, yes, CEFs.

All told, it hands you $8,000 in yearly dividend cash for every $100K invested!

So if you invest, say, a $500K nest egg, you’ll get back $40,000 a year in income. And with that cash dropping into your account every month ($3,333 a month, to be precise), you won’t have to lift a finger!

Your cash will come in, your expenses will go out—and you’ll be left with a nice surplus “on the side,” which you can spend however you like (or reinvest, building your income stream further).

Full details on these stout income plays are waiting for you here. You’ll discover:

- An 8.1% payer that’s set to rake in huge profits from an artificially depressed sector.

- The brainchild of one of the top fund managers on the planet that’s giving out a generous 9.1% yield.

- And a rock-steady 6.9% dividend trading at a massive discount to NAV.

Don’t miss your chance to start tapping this life-changing dividend stream while you can still get in at a bargain. I’ll share all the details on every stock in my “8% Monthly Dividend Portfolio”—names, tickers, buy-under prices and much more—with you right here.

Source: Contrarian Outlook