The vast majority of the time in a wishy-washy market environment like the one we’re in now, “buying the dips and selling the rips” is an appropriate strategy.

Traders can count on a reversal when a rally or meltdown becomes overextended.

In some cases, though, a sharp stumble isn’t necessarily a buying opportunity. Rather, it’s a glimpse at the shape of things to come, with investors only beginning to file out of an equity.

With that as the backdrop, here’s a closer look at 10 oversold stocks to sell rather than scoop up at their currently depressed prices.

While investors should remain on guard for rebounds inspired by bargain-hunters expecting the reversals we’d normally see in such situations, in all of these cases we’ve seen a handful of red flags suggesting things could get worse before they get better.

In no particular order…

Stocks to Sell: J B Hunt Transport Services (JBHT)

It wasn’t a disastrous quarter, but last quarter’s numbers from J B Hunt Transport Services (NASDAQ:JBHT) were far from being impressive. More than that, they may be a microcosm of a bigger headwind that’s now blowing.

One issue, ironically, is that the economy is so strong and jobs are so plentiful, trucking companies like J B Hunt are struggling to find and keep drivers. Then there’s slowing demand for intermodal transportation, mostly crimped by trade friction between the U.S. and China. Earnings of $1.09 per share fell short of the $1.26 analysts were expecting.

That lackluster future is still being priced into the chart. Though down by nearly one-fourth since June’s peak, JBHT shares have yet to slide back to a long-term support line, currently at $83. The current trend pushing shares that direction has plenty of momentum too.

Mattel (MAT)

To its credit, toymaker Mattel (NASDAQ:MAT) has done its best to adapt to an electronic, digital world. In January, Chief Technology Officer Sven Gerjets demonstrated the company’s deep understanding that the future is ‘phygital’ … the melding of traditional physical toys with computerized technology. The company is thinking aggressively about media tie-ins too, reportedly planning a live-action film featuring Mattel’s beloved Barbie doll.

For whatever reason, though, nothing really seems to be clicking for the once-iconic company. Though MAT stock looked like it would finally work out a reversal after December’s hard landing, the selling that got started back in 2014 has been renewed this month. The stock is down nearly 70% from the peak made five years ago, and once again within easy reach of multi-year lows.

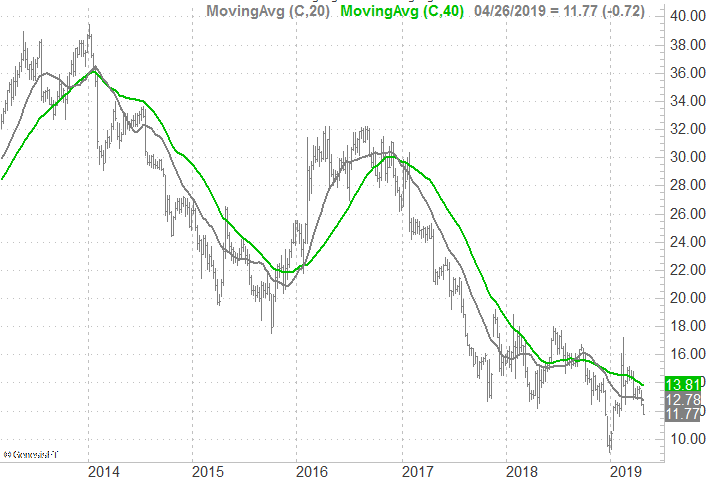

Gilead Sciences (GILD)

When Gilead Sciences (NASDAQ:GILD) shares tumbled in 2016, investors largely knew why. An amazing run in 2013 and 2014 stemming from sky-high prices of its hepatitis C drugs Harvoni and Sovaldi — which were effectively ‘cures’ — were about to be challenged by cheaper competitors as well as social outrage over their needlessly high price tag.

By early 2017, though, investors figured the worst had been priced in and assumed Gilead would properly regroup for the road ahead.

That hasn’t turned out to be the case though. GILD stock has been steadily trending lower since its early 2018 high, and if shares break below a technical floor right around $60, this oversold name will most definitely become one of a handful of stocks to sell.

In short, Gilead Sciences simply isn’t holding up to its competition.

Nordstrom (JWN)

It’s sometimes difficult to tell given the number of store closing we’re still seeing, but the so-called retail apocalypse is abating. That’s a big reason Nordstrom (NYSE:JWN) rallied in 2018. For a short while, it appeared as if the upper-end chain of stores would emerge from the industry-wide meltdown as healthy as it has ever been.

It’s now clear, however, that while not as brutal, the retail apocalypse is still underway, and still plaguing some slivers of the business more than others. Last quarter’s total top line of $4.48 billion was not only down from the year-ago tally of $4.7 billion, it also fell short of the $4.61 billion analysts were expecting. Same-store sales at its full-priced venues was a scant 0.1%.

JWN is already one of several oversold stocks in the sector. But, if it breaks below the support line that tagged the 2016 and 2017 lows, it will earn a spot on a short list of stocks to sell.

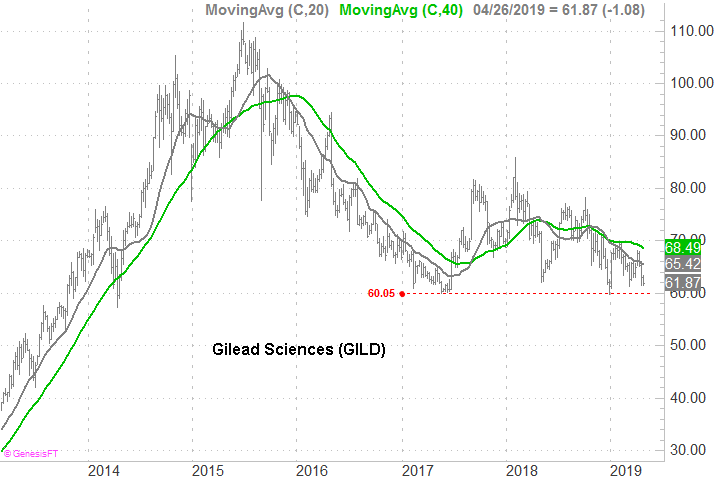

Wells Fargo (WFC)

Wells Fargo (NYSE:WFC), to be clear, is mostly suffering from self-inflicted wounds. The 2016 account-opening scandal led to backlash from multiple directions ever since.

The public — consumers — was at least willing to forgive if not outright forget. A surprising string of quarterly results carried WFC stock to record highs by early 2018.

That’s when regulators really started to sink their teeth into the company’s hide though. Among other things, the mega bank in August was charged more than $2 billion for making improper mortgage loans. The clincher, however, is the fact the Federal Reserve has capped the company’s permitted assets it can leave on the books, essentially capping earnings growth. The company doesn’t believe that growth ban will be lifted anytime this year.

With little to look forward to, WFC shares are in a well-developed downtrend that probably won’t find a firm floor until it reaches the $41 area.

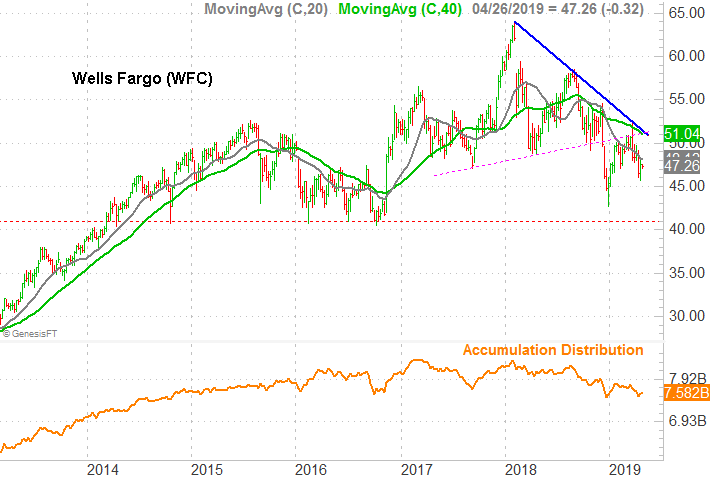

L Brands (LB)

L Brands (NYSE:LB) shares are down a stunning 69% from their late-2015 peak, and that downtrend is still going strong. The stock is only a few pennies away from new multiyear lows, and given its bearish momentum, odds are good it will once again slide deeper into the red.

L Brands, of course, is the parent company of Victoria’s Secret and Bath & Body Works … two powerhouses in the heyday of mall shopping, but two venues that are struggling to connect with consumers in a digital world where shoppers splurge in different ways. While revenue growth remains steady, quarterly operating income has been reliably shrinking since early 2016 as L Brands has to spend more and more to keep patrons coming to its stores. And even then, things are tough. Fourth-quarter same-store sales excluding e-commerce spending was down 1%, extending a concerning streak of backpedaling.

In that light, the stock’s long-term downtrend makes sense.

AbbVie (ABBV)

AbbVie (NYSE:ABBV) was a heroic performer in 2017, rallying from $57 to an early 2018 peak near $117, mostly driven by impressive sales growth from Humira as well as Imbruvica. The former’s revenue was up 14.4% that year, and the latter’s grew more than 40%.

The big run-up only set up a sizable fall though, spurred not by slowing revenue growth, but an impending and inevitable threat to its Humira franchise.

The company has been maneuvering for years to maintain the patent on its flagship drug Humira, to be clear, which generated nearly $20 billion in revenue last year. But, time is ultimately working against AbbVie. Earlier this month six separate lawsuits were filed against the pharmaceutical giant, each making the same basic claim … that biosimilars of Humira should already be allowed in the United States.

Investors appear to know the company won’t be able to fend off these legal arguments for much longer.

Nektar Therapeutics (NKTR)

In late 2017, the Nektar Therapeutics (NASDAQ:NKTR) rally was unstoppable. Eli Lilly (NYSE:LLY) had made an upfront cash payment to the company in exchange for development and participation rights in T-cell booster NKTR-358, and at the same time posted big-time third quarter revenue growth.

As is so often the case in the biopharma arena, though, excited investors overestimated what was to come, and how quickly that would take shape. In June of last year a trial of cancer therapy NKTR-214 led to lackluster results, and in February the company once again reported just so-so outcomes with the same drug in use as a therapy for a different form of cancer.

Nektar Therapeutics shares have fallen more than 70% since their early 2018 high, and are pennies away from breaking below an established support level of right around $30.

HP (HPQ)

After a brief stumble in 2015 when it split with the enterprise-oriented half of the company Hewlett Packard Enterprise (NYSE:HPE) to focus on consumer-level computers and printers, HP (NYSE:HPQ) started what would turn into a solid, multiyear advance. The early-2016 low near $8 gave way to a move to 2018’s peak near $27, partially driven by steadying PC sales, and partially prompted by an improving economy.

That 2018 peak, however, has also become a perfect pivot. Since then HPQ shares have logged a lower major low and lower major high, and as of this week appear to be aiming at a new 52-week low. Traders aren’t buying on the dip — at least not in earnest — now that the bullish trend lines of yesteryear have been snapped.

Davita (DVA)

Finally, add Davita (NYSE:DVA) to your list of oversold stocks to sell rather than buy. Though down 36% from its early 2018 high, there’s still room and reason for it to continue sinking.

It may not be a household name, but it may ring a bell all the same. Davita is a chain of kidney care and dialysis centers that for years had been one of Warren Buffett’s favorite stock picks. The company was a reliable cash generator … right up Buffett’s alley.

Buffett, through Berkshire Hathaway, still owns a big stake in Davita, but arguably wishes he didn’t. Operating income turned unpredictable beginning in 2012, and in 2017 began to shrink more often than grow. That headwind has been reflected in the stock’s price from the point in time it started to blow.

Buffett and Berkshire appear to still be committed to the trade. Given the uncertain future the country’s healthcare system faces though, on top of the trouble the company was facing even before such questions surfaced, there’s no end in sight for the stock’s net-bearishness.

— James Brumley

If you're buying rare earth or other critical mineral stocks, you're already one step behind - because we believe that political insiders in Washington are preparing to buy a whole new group of stocks, which could begin soaring 500%+ just days from now. The man once ranked in 2020 as America's #1 stock picker is doing something extraordinary and giving away the name and ticker of every single stock that could be next. Everything you need to know is here.

Source: Investor Place