With the market taking a pause after rallying more than 5% off the May 3 low, the question every investor has to contend with is: Does the rally have more steam… or is a pullback imminent?

With the 10-year yield above 3% and global trade issues resurfacing, the argument for the latter has merit.

But there’s one technical indicator I follow that’s flashing a bullish sign; it tells me more upside is likely.

Small-cap leadership is an indication of a healthy market.

I consider it a reliable “risk-on” indicator that reflects investor willingness to buy stocks based on a perceived increase in risk value.

More risk here adds up to more reward…

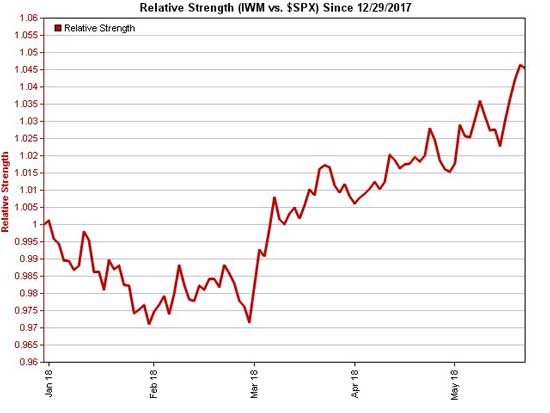

Strong Bull Markets Are Led by Small-Cap Stocks

And that’s exactly what we’ve been seeing for the past three months, as shown in the chart below.

In fact, since April 2 – the only day the S&P 500 closed below its 200-day moving average since June 2016 – the small-cap iShares Russell 2000 ETF (NYSE Arca: IWM) has gained 9.8% compared to the S&P 500’s 7.0% and 8.1% from the Nasdaq.

Now, I’ve been saying for at least a week that my “Best in Breed” ETF ranking system is pointing to the energy, oil, and oil services sectors as leaders in this market.

Now, I’ve been saying for at least a week that my “Best in Breed” ETF ranking system is pointing to the energy, oil, and oil services sectors as leaders in this market.

I combed my database and found the following two small-cap stocks in those sectors that should continue their recent outperformance.

These Have the Biggest Potential Payoff for What You Risk

California Resources Corp. (NYSE: CRC) is a small oil and gas explorer/producer based in Los Angeles.

The stock has been a monster performer of late, nearly tripling in value from mid-March to a two-year high this week. Along the way, the company benefited from a slew of price target increases after releasing an upbeat earnings report earlier this month.

But despite the huge rise, the party may not be over for CRC shares just yet. Although the stock pulled back on Wednesday, there are a couple of reasons to believe there’s more fuel in the tank.

Short interest has been on the rise since January, even though the stock is up 88% in 2018. With a short-interest ratio above 7 and the shares shooting higher, the shorts will have to cover their losing bets sooner rather than later.

The Street is likewise skeptical, as just a quarter of the covering analysts rate California Resources a “Buy.” But that’s an improvement from a month ago, when nobody thought of the stock as a buy. This could be the beginning of an analyst rush to upgrade a stock that has few performance peers this year.

With high short squeeze and upgrade potential, CRC should be looking at a target of at least $50 within the next month.

I’ve got another one for you…

I’ve got another one for you…

Diamond Offshore Drilling Inc. (NYSE: DO), which provides contract drilling services through a fleet of offshore drilling rigs, drillships, and semisubmersibles.

Though the stock is up only slightly for the year, it’s gained an impressive 37% off the April 2 low.

The shares have been consolidating for the past two weeks along their gently ascending 20-day moving average. Despite the sideways pattern, Diamond hit a 17-month high this week. Also, the 50-day moving average, which sits below the share price, is in a strong incline, a bullish sign.

The shares have been consolidating for the past two weeks along their gently ascending 20-day moving average. Despite the sideways pattern, Diamond hit a 17-month high this week. Also, the 50-day moving average, which sits below the share price, is in a strong incline, a bullish sign.

While Diamond’s chart may be less impressive than that of California Resources, the short interest and analyst pictures are much more one-sided. Short interest has been stair-stepping higher for more than 18 months, resulting in a squeeze-inducing short-interest ratio just below 12.

The analyst community is aligned even more against DO, with just three of the 32 covering the stock rating it a “Buy.” Clearly there is huge potential for short covering and analyst upgrades, which should propel the stock above its January high to a near-term target in the $22 area.

— Chris Johnson

Source: Money Morning