Lately, I’ve heard more real estate bulls touting rental property as the perfect retirement investment.

Truth be told, it can be.

You probably know people who’ve built a nice income stream in their golden years from a well-chosen set of rentals.

Trouble is, there’s a big—and too-often glossed over—problem with being a property baron: it’s not the easy ride housing fans make it out to be!

That is, unless you like being on duty 24/7 to fix clogged toilets, chase down deadbeat tenants and deal with noise complaints.

I don’t know about you, but that’s not how I plan to spend my golden years.

Less Work, More Profits

But don’t worry; there is a way to grab those steady rent checks without taking on a second job.

The key isn’t owning physical real estate, but instead making your property buys through real estate investment trusts (REITs), which own income generating properties—everything from apartments to self-storage units.

(In just a few paragraphs, I’ll share 2 trusts set for big gains in 2018. Each throws off a gaudy yield of 4.7% or more—and one has doubled its payout in the last 5 years alone!)

One of the best things about REITs is that they trade on the stock market, so you won’t get soaked on real estate commissions—you’ll only pay the small trading fee your online broker charges.

REITs Will Surge in ’18—Thanks to Trump and the Fed

Here’s the best news: today, we’re staring at two things that are poised to make 2018 the year REITs finally break out and explode for double-digit gains.

The first? The new tax law, which, as I told you in a December 27 article, classifies REITs as “pass-through” investments.

Translation: if you’re in the top tax bracket, the bill on your REIT dividends just dropped to 29.6% from 39.6%.

First-level investors haven’t realized just how big a deal this is. When they do, they’ll pour into the REIT space, setting us up for some nice price upside.

And don’t forget, REITs already get a terrific advantage, even without the new tax plan: they pay no corporate tax at all, so long as they send out 90% of their taxable income to investors as dividends.

That’s why REITs’ payouts are so high. As I write, the benchmark Vanguard REIT ETF (VNQ) yields 4.5%, and there are plenty of trusts—like the 2 I’ll show you in a moment—paying much more than that.

(I should also mention here that at the very end of this article, I’ll give you a chance to unlock my No. 1 REIT pick for 2018. It sports a gaudy 10.1% forward yield and grows its payout every single quarter).

Cashing in on the Herd’s Fear

My second reason why now is the time to buy? REITs are cheap, thanks, again, to a flaw in the herd’s thinking, this time about higher interest rates and REITs—namely, that the former is terrible news for the latter.

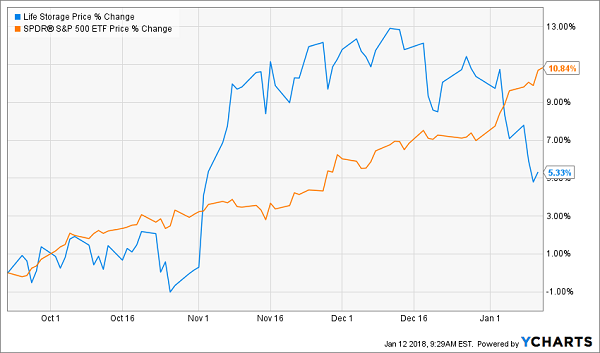

Here’s how that’s shown up in the performance of the benchmark Vanguard REIT ETF (VNQ) in the last month:

Snapshot of an Overblown Fear

I hope you’re not one of these nervous Nellies, because the so-called “wisdom” on REITs and interest rates is totally backwards: in the long haul, rising rates are good for REITs because they signal a stronger economy. That brings higher rents and surging demand for rental space. Compared to that, a small rise in REITs’ interest costs is peanuts!

I hope you’re not one of these nervous Nellies, because the so-called “wisdom” on REITs and interest rates is totally backwards: in the long haul, rising rates are good for REITs because they signal a stronger economy. That brings higher rents and surging demand for rental space. Compared to that, a small rise in REITs’ interest costs is peanuts!

It’s been proven time and time again, including when REITs pummeled the market in the last rising-rate period in 2004–06.

So what’s the bottom line here?

Simple: it’s time for us to get greedy for yield—and the 2 bargain-basement REITs up next are a great place to start.

Bargain REIT No. 1

Physicians Realty Trust (DOC): One thing REIT investors get that rental-home owners can only dream of is instant access to tough-to-access corners of the market.

Case in point: DOC, which has 262 medical office buildings rented out to doctors, hospitals and health care systems, mainly on the east coast and in the Midwest.

This is a terrific business to be in as baby boomers age and need more medical care.

One thing I love about DOC is its long tenant list, with no one client chipping in more than 5.5% of annualized base rent. That means DOC isn’t leaning too hard on one operator—a common trap that can snare other healthcare REITs.

A Diversified Portfolio

DOC’s steady rent checks translate into rising funds from operations (FFO; the REIT equivalent of earnings per share): in the last 12 months, the trust’s normalized FFO has come in at $1.05, up nicely from $0.96 in the previous period.

DOC’s steady rent checks translate into rising funds from operations (FFO; the REIT equivalent of earnings per share): in the last 12 months, the trust’s normalized FFO has come in at $1.05, up nicely from $0.96 in the previous period.

It’s a short hop from there to the trust’s rich dividend payout, which yields a gaudy 5.5%. And before you ask, yes, that payout is safe, accounting for a very manageable (especially for a well-run REIT like DOC) 86.7% of FFO.

Finally, you can buy in at just 15.9-times FFO today, way down from 19.3 a year ago. That’s a great deal, given DOC’s top-notch portfolio and upside.

Bargain REIT No. 2

Life Storage (LSI) soared 13% in a little more than two months after I recommended it on September 23, but it’s pulled back since then, thanks to recent REIT pessimism; it’s now up just 5.3%.

Storage REITs also got roughed up last year due to worries about oversupply. But the folks at Life, with 700 self-storage facilities in 28 states, clearly didn’t get the memo! The trust ended the third quarter with record occupancy of 92.7%.

Add it all up, and you get a nice second chance to buy here.

Buy Window Opens Again

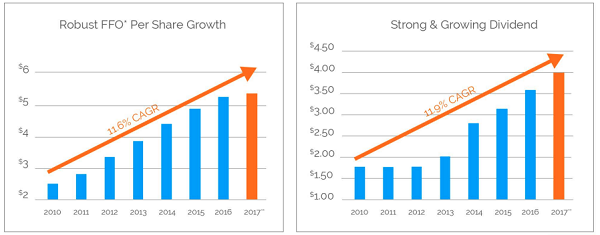

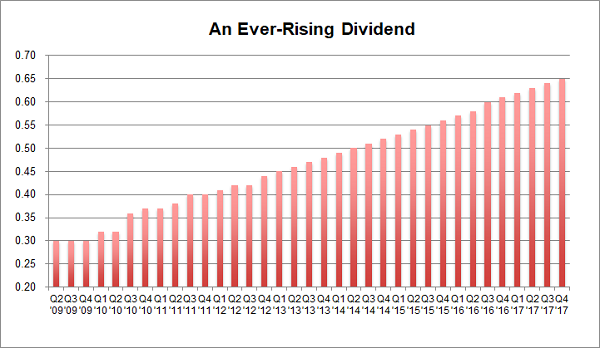

Something else you’ll love about LSI? You not only getting a nice 4.7% current dividend, but management is growing the payout in lockstep with FFO, and has more than doubled it in the last 5 years.

Something else you’ll love about LSI? You not only getting a nice 4.7% current dividend, but management is growing the payout in lockstep with FFO, and has more than doubled it in the last 5 years.

A Consistent Dividend Grower

The great thing about self-storage is that it benefits from many unstoppable trends, like downsizing baby boomers; millennials’ avoidance of homeownership (and related need for more storage); and the rise of Amazon.com (AMZN), which gives us yet another way to acquire more stuff!

The great thing about self-storage is that it benefits from many unstoppable trends, like downsizing baby boomers; millennials’ avoidance of homeownership (and related need for more storage); and the rise of Amazon.com (AMZN), which gives us yet another way to acquire more stuff!

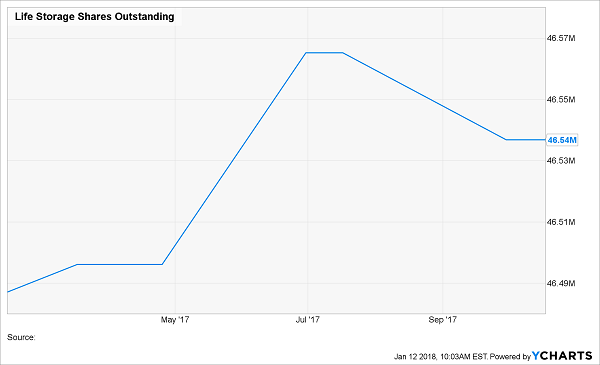

The kicker? Thanks to the pullback, Life trades at a reasonable 15.8-times adjusted FFO, a bargain valuation that’s prompted Life’s board to authorize a $200-million buyback plan, which management has swiftly put into action.

Buy Alongside the Company

That may not look like much of a drop in the share count, but it’s a big deal for REITs, which are notorious for issuing new shares to finance property purchases and renos.

That may not look like much of a drop in the share count, but it’s a big deal for REITs, which are notorious for issuing new shares to finance property purchases and renos.

— Brett Owens

My Top REIT Pick for 2018 (10.1% dividends and 20%+ GAINS this year) [sponsor]

My top REIT pick for 2018 boasts an even higher dividend than the 2 trusts above (an eye-popping 10.1% forward yield!). And as I mentioned earlier, it grows its payout every single quarter.

In fact, this powerhouse REIT has increased its dividend for 21 straight quarters, and we’re locked in for 4 more dividend hikes in 2018!

Here’s the truly unbelievable part: this one of the cheapest REITs I’ve run across in years, trading at a rock-bottom 10 times FFO!

Here’s the truly unbelievable part: this one of the cheapest REITs I’ve run across in years, trading at a rock-bottom 10 times FFO!

I know what you’re thinking: a proven dividend payer like this, trading at such a ridiculous markdown, is just too good to be true.

Well, guess what? It is.

Which is why I expect this stock’s valuation and price to rise 20% in 2018 as the herd finally clues in to the benefits rising rates and the new tax plan will shower on REITs.

That’s why I’ve made this unsung REIT pick a cornerstone of my “8% No-Withdrawal” portfolio, a collection of 6 investments from every corner of the market that I’ve assembled to do one thing (two, actually):

- Deliver a safe 8% average dividend: That’s enough to pay you $40,000 in income—enough for many folks to retire—on a $500,000 nest egg.

- Safeguard your retirement stash, letting you fund your golden years on dividends alone without drawing down your nest egg! This insures your retirement against a market meltdown and lets you leave a lasting legacy for your kids (and grandkids).

I’m ready to share the names of all 6 stocks and funds inside this dynamic portfolio with you now. Click here to get the name, ticker symbol and full details on my top REIT pick and all 6 of these perfect retirement investments now.

Source: Contrarian Outlook