There is no subject I’ve shared with you more than the ongoing global economic recovery. Nearly every corner of the globe is enjoying economic growth – the first such synchronized period since before the global economic crisis of 2008-09.

Thanks to global growth and the loosening of regulation by the Trump Administration, many of America’s industrial companies (and its workers) are enjoying a renaissance.

For example, in September, U.S. manufacturing expanded at its fastest pace in 13 years as measured by the Institute for Supply Management’s factory index.

The trend showing strength in American manufacturing is likely to continue since a gauge of customer inventories remains near six-year lows.

And the order backlog index remains near the September figure, which was the highest level since April 2011.

That’s good news for workers, who have already felt the effects of the rebound.

In the past year, more than 156,000 workers have found employment in U.S. manufacturing. That’s a sharp contrast from the final year of the Obama Administration when 16,000 manufacturing jobs were lost.

This confluence of factors is what makes the industrial sector my second-favorite sector for 2018, trailing only technology.

Industrial Companies Nirvana

I believe conditions now for industrial companies are the best they’ve been this century. And executives at of some of America’s largest manufacturers agree.

Inge Thulin, CEO of manufacturing powerhouse 3M (NYSE: MMM), said in the company’s latest conference call, it was “good to see broad-based growth across all geographic areas.” Thulin added the company had “very high confidence as we move into 2018.”

There were similar statements from many executives in the sector. However, not every industrial company is enjoying the good times. You need look no further than very troubled General Electric (NYSE: GE) to know that.

Of the 10 largest industrial companies in the S&P 500 index, only three of them recorded higher third-quarter earnings per share than the year earlier period. So you can’t just throw a dart and pick out any industrial firm.

Good management is needed. Such as at the only three aforementioned companies that reported good earnings – 3M, Caterpillar (NYSE: CAT) and Honeywell (NYSE: HON). Or other manufacturing firms that beat earnings expectations including United Technologies (NYSE: UTX) and General Motors (NYSE: GM).

3 Industrial Stock Investments

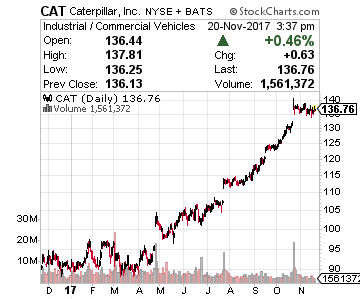

One prime example of a company enjoying what is going with the global economy is Caterpillar.

One prime example of a company enjoying what is going with the global economy is Caterpillar.

It is the world’s leading manufacturer of construction and mining equipment, and also makes diesel and natural gas engines and industrial gas turbines.

The company reported third quarter global sales rose 19%, marking the fastest pace since 2012.

It also projected 2017 sales of $44 billion, marking a third straight increase in its annual revenue forecasts.

But what should stand out to you was the breadth of demand for its products, which almost looked tech-like.

Sales surged 27% in North America as the U.S. shale oil and gas industry cranked up again. Meanwhile, China’s growing construction market helped sales in the Asia Pacific region balloon 31%. Dealers’ replenishing of inventories boosted sales in Europe, Africa and the Middle East by 22 % and “stabilizing economic conditions” in Latin America lifted sales by 24%.

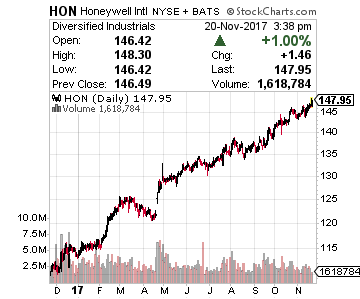

Another great example of an industrial company doing well is the industrial conglomerate Honeywell.

Another great example of an industrial company doing well is the industrial conglomerate Honeywell.

Its revenues breakdown by division is as follows: aerospace – 36.1%, performance materials – 22.3%, home and building technologies – 27.6%, safety and productivity solutions – 14%.

This company was on the brink of failure in 2001 until the recently-retired David Cote took over as CEO.

The turnaround he engineered is evidenced by the stock haven risen fivefold since then, excluding dividends.

I like the fact that Honeywell is increasing its exposure in fast-growing regions of the globe like China and India.

The developing world offers huge growth opportunities across its portfolio of products. For example, Honeywell paid $5 billion for Elster, a leading provider of thermal gas solutions (as well as water and electric meters) across industrial and residential uses. Infrastructure investments as well as increasing gas consumption in those regions will boost the Elster business.

Honeywell’s stock is still cheap too. Its P/E of 19 is still well below that of other premier industrial firms such as 3M, whose P/E is 27.

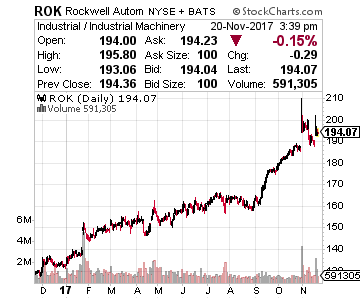

Finally we have my favorite pick in the sector, the first stock that I added to the Growth Stock Advisor as editor in May – Rockwell Automation (NYSE: ROK).

Finally we have my favorite pick in the sector, the first stock that I added to the Growth Stock Advisor as editor in May – Rockwell Automation (NYSE: ROK).

Since being added to the portfolio, its stock has soared by nearly 25% in just six months.

The company sits in the sweep spot of the $200 billion factory automation market, selling factory hardware and software to manufacturers around the world.

And it is enjoying global growth. Its CEO Blake Moret recently told analysts that “Global macroeconomic conditions are solid and cited “strong orders” for the company.

Rockwell expects organic sales growth as high as 6.5% in its 2018 fiscal year, with an added 2.5% to be provided by the continuing weakening of the U.S. dollar.

For those of you unaware, Rockwell Automation recently became the target of an unfriendly bid from Emerson Electric (NYSE: EMR). Emerson is a slow-growing industrial conglomerate desperate for the growth that Rockwell has. That is evidenced by now the third such bid in recent weeks – an offer now of $29 billion or $225 a share, with $135 in cash and the rest in Emerson stock.

I hope that the management at Rockwell Automation continues to reject the deal, which is not good for shareholders. If they do eventually sell, hopefully it is to another high-quality company like Honeywell.

— Tony Daltorio

[ad#ia-tim]

Source: Investors Alley