According to Time.com, more than 50% of Americans age 35-54 have less than $10,000 saved for retirement. How we got to this point over the last 15 years is hardly surprising.

In the wake of the Great Recession, many people saw their 401(k)s wiped out, and they lost a lot of faith in the financial markets. Members of Generation X lost 45% of their average net worth during the financial crisis, according to the Financial Times.

If you find yourself in this group, let me start by reminding you of two things:

First, you are not alone. Millions of Americans are in the same situation.

Second, you have plenty of time to start building or rebuilding a retirement nest egg that’ll put you on your way. According to retirement experts, most Americans have time to catch up and reach their retirement goals.

If you’ve already started saving money, consider yourself ahead of the game. But you still need to set aggressive goals if you want to retire at 60.

Get started with these immediate steps.

Step No. 1: Capitalize on These Underused Retirement Benefits

A majority of Americans are making the mistake of not using their IRA and 401(k) options at work.

In 2017, you can put up to $18,000 into a 401(k) account – all of which does not count toward your adjusted gross income (AGI) when you file your taxes each year. Also, many employers have matching contributions, in which they will meet as much money as you put into your account up to a specific percentage.

Simply put, this is free money for your retirement, and it can reduce your taxes.

On the IRA side, you have two options:

You can open a Traditional IRA or a Roth IRA (though the latter has income maximums to qualify). It is recommended that you put aside at least 10% to 20% of your income or more into an investment savings account. Remember, the sooner that you begin investing in these accounts, the sooner you will start to benefit from compound interest and long-term stock appreciation.

If you currently live on $80,000 per year, for example, and want to maintain your standard of living, you will require roughly $2 million in assets by the time you retire.

To reach this goal, you may want to start putting away 10% to 20% of your paycheck each month, depending on where you are in your 40s.

If you have maxed out your 401(k) and IRA, you may also consider investing your money in another account and starting to invest in stocks and bonds that pay high yields.

This strategy will require discipline, so we advise that you consider an automatic payroll transfer into a retirement account.

If your money is not in your checking account, you’ll face less temptation to spend it. Also, be sure to put away any additional raises or bonuses that might come along. This strategy will help reduce your annual tax burden and shore up the savings deficit you may find yourself in these days.

Each year, you should aim to boost your savings a little more. Here’s the math:

- Suppose you earn $50,000 and put away 10% in the first year.

- Each year you gradually boost your savings on that $50,000 by 1% through the decade.

- By the end of 10 years, you would have saved $72,500 of the $500,000 you would have earned over the decade. Assuming a 6% return, that account would be worth $92,955.

- After another 16 years, the money you saved in your 40s (at a 6% rate of return) will be worth $248,870. And that is assuming that you have earned no additional money during that time.

Action to Take: Contact your employer’s Human Resource department – or your respective 401(k) and IRA personnel. Make sure you’re fully capitalizing on any matching programs they provide, and consider an automatic payroll transfer if the opportunity is available to you.

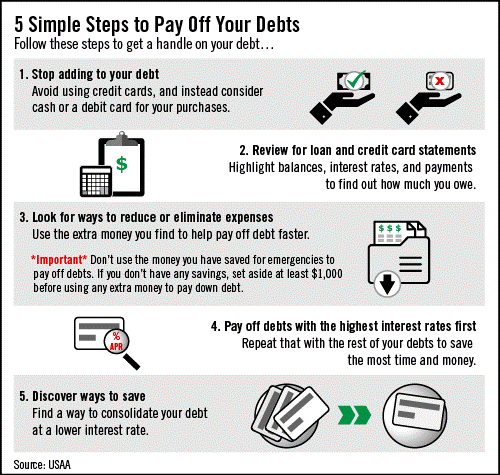

Step No. 2: Cut Thousands of Dollars Over a Decade with This Debt-Elimination Plan

While you’re putting money in your retirement accounts, you also must balance your debt obligations. If you have large balances, it’s critical to start paying off your highest-interest debts, like credit cards, or to find ways to refinance those loans and debts to reduce those interest costs.

The current average rate for a variable rate credit card is higher than 15% a year, according to BankRate.com. Also, student loans from decades ago could have interest rates higher than 8%, depending on when they were accessed. There’s also the option of refinancing your mortgage loan.

According to Black Knight Financial Services, there were more than 8.7 million refinancing candidates nationwide in 2016, but only a fraction of those applied.

Remember that you don’t need to make a huge push to pay off your mortgage. In addition to potential appreciation in your home price, you can also refinance your mortgage and subtract interest from your taxable income if you itemize your deductions.

A $250,000 mortgage from 2015, refinanced from 4.5% to 3.5% in 2016, would have saved $75,000 in mortgage interest costs over the life of the loan.

While you’re looking for ways to shrink your debt burden, it’s also important to consider the means to cut back on spending. Some Americans will spend $5 per day on a coffee drink from a local barista. That can add up to more than $1,500 a year.

That’s a big chunk of change back in your pocket merely from cutting back on your daily Starbucks fix.

Or it could be as simple as swapping out a light bulb.

According to the latest data from the U.S. government, the annual energy bill for a typical single home is spent mostly on electricity. In fact, electricity accounts for roughly 9% of total household budgets. Luckily, there’s an easy way to cut that number down.

Switching just one old-school incandescent bulb to a newer compact fluorescent (CFL) or light-emitting diode (LED) model can save you up to $95 or more over the lifespan of the bulb. If you’re like the average American household, you may still have 50 or more money-wasting bulbs burning away your hard-earned cash. Switching all of them over to newer, more efficient technology can save you over $4,700 – more than enough to nicely pad your retirement portfolio.

The adage is that you can be a producer or a consumer. If you’re looking ahead to your retirement, you want to be producing more than you consume. So look for ways to cut back. Make it a game if you can. Every dollar you save is a dollar that can be allocated not only to savings, but to boosting your retirement income for years to come.

— Keith Fitz-Gerald

[ad#mmpress]

Source: Money Morning