Let’s talk about five big payouts that are so flimsy, they’re just asking for the ultimate sign of dividend disrespect:

Paying money to short them.

It’s one thing to turn down a decent yield in today’s 2% world. It’s another to be willing to pay the dividend in order to bet against the stock!

Yet here are five firms with archaic business models (some are so-2015) that their cash flow streams will soon dry up. And when the cash evaporates, so will the dividend.

Which is why I may short some or all of these shares in the weeks ahead after this piece publishes. I personally have no problem paying these “dividend taxes” for the right to bet against these stocks – because I don’t expect the levies to remain high for long!

Shorts are often scared off by dividends. This can make the post-cut plunge all the more painful (with no shorts there to cover, or buy back, their initial positions).

I probably don’t need to remind you what happened recently to Mattel (MAT) or Teva (TEVA). (The former was featured in my Dirty Dozen report warning about dividends most likely to be cut.) Both were favorites of first-level income investors and the Internet pundits they followed.

Unfortunately these headline followers all learned the hard lesson that stock prices eventually follow their dividends in both directions:

Two Recent Dividend Disasters

The damage has been done here. But plenty of dividends that would have been considered safe in yesteryear are now “on the clock” for cuts of their own.

Here are five payouts that are being eaten alive by Amazon (AMZN) and the broader Internet. I’d sell them now (or even short them outright).

5 Dicey Dividends I’d Sell (or Short) Today

Buckle (BKE) is a shareholder-friendly retailer that got caught in no man’s land when retail ended. Management pays a regular quarterly dividend plus big special dividends every year.

In hindsight, management should have been saving its money and reinvesting in mobile shopping and other ways to connect directly with its customers. At this point, it’s probably too late. Revenue is in a downward spiral, with the share price following:

Buckle’s Shares Buckle

The quarterly dividend should have been cut two years ago. And those big special dividends (shown by the orange spikes above) should have been invested somewhere smartly. But it wasn’t, and it’s now only a matter of time until Buckle’s dividend officially buckles with the firm paying out 83% of its declining profits to shareholders.

Up the chain, Macy’s (M) is finished as well. The department store has been replaced by web browsers and mobile apps, and this firm didn’t connect directly with its end customers in time either.

Macy’s has finally halted its dividend increases – next up will be the drop. It should have happened already, but management has kicked the can down the road.

Macy’s Dividend Mirage

My only hesitation with shorting shares right now is that short interest is steadily climbing, so it might be best to look for a “dead cat bounce.” Regardless, this 7% yield is not worth the risk from the long side.

DineEquity (DIN), owner of Applebees and IHOP, makes a dubious return visit here. I warned you about these shares just over two months ago, and they’re already 14% lower:

Down 14% Since Our July Warning

DineEquity had been a generous dividend payer (and grower to boot). Problem is, the restaurant business today is a zero sum game. For every Applebees, there are countless food delivery boxes being delivered to the same local neighborhood.

The next move will be a dividend cut. Its 9.7% yield, a product of a tanking stock price, is not sustainable. The company is paying out 84% of its declining profits to shareholders, and it badly needs the money to attempt to figure something out.

Cracker Barrel (CBRL) is better run, but in the same sinking boat. Its stock, fundamentals and dividend have held on until this year. But it’s now paying nearly all (95%) of its profits as payouts, which is way above its historical norms.

Skyrocketing payout ratios are often ominous. In Cracker’s case, it doesn’t look to be a passing thing, either:

A Price Powered by Payout Ratio (Not Good)

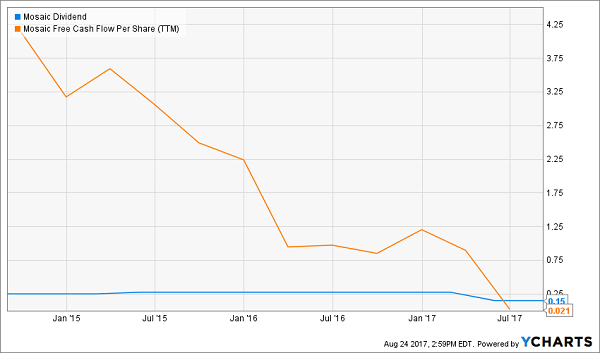

Finally fertilizer maker Mosaic (MOS) remains behind the dividend cut curve. Low agricultural prices have crushed its profit margins (and free cash flow). The firm has already chopped its payout once in 2017 – one more will happen soon if business doesn’t turn around:

Mosaic is Due for One More Dividend Cut

I warned you about Mosaic for the first time last November (before its first cut) – it’s down 28% since. We revisited in March, when I warned another dividend drop was on the way. That hasn’t happened yet – but its stock is already dropping in anticipation of the bad news.

Don’t get cut trying to catch these falling knives.

— Brett Owens

This Friday: 7 Dividend Buys Paying 8.4% [sponsor]

I don’t mess around with expired business models. Nor do I waste time with paltry 2%, 3% or even 4% dividends.

This Friday, I’ll be outlining my seven top dividends to buy right now. All of these payouts are well funded, and likely to grow in the future.

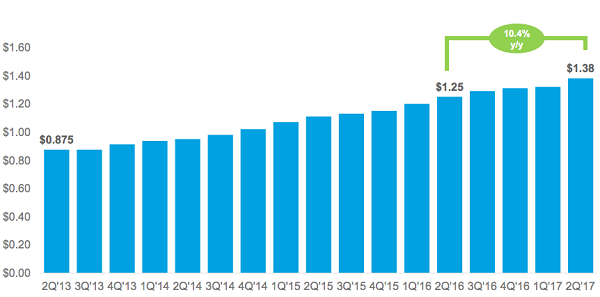

My favorite firm has now increased its payout every quarter for 16 consecutive quarters. And these have been meaningful increases with sustained momentum. The company’s most recent hike represented a 10.4% increase year-over-year:

An Accelerated Aristocrat: 16 Straight Hikes

The best time to buy a dividend grower like this is anytime. But we can tip the odds in our favor even further when we buy at moments like these – when the share price is due to “catch up” to the dividend.

There have been two great times to buy these shares in the last five years:

- Early 2016. Its stock price plunged below its ever-growing dividend, providing opportunistic investors with quick 35% price upside. And,

- Right now.

Stocks tend to appreciate as fast as their dividends. Buy a static payer, and you shouldn’t expect much upside. Buy a 10% annual dividend grower like this, and you should expect 10% price upside to go along with your 7.7% yield.

Remember, total returns are made up of dividends and price appreciation. The latter, price gains, are driven by some combination of:

- Dividend raises (which inspire investors to pay more for the stock or fund), and/or

- A climb towards fair value (a closing of the discount window in a closed-end fund’s (CEF’s) case, or a higher multiple on FFO for a REIT).

All together, my dividend superstar 7-pack yields 8.4%. And each issue has price upside to boot – giving us the potential for 15% to 20% total returns in the year ahead.

Since inception, my 8% No Withdrawal Portfolio has returned 13.6% annualized (and paid 7%+ in dividends) versus just 10.5% for the S&P 500 during the same time period. Proving that you don’t have to choose between yield today and total returns tomorrow – you can have both!

My top seven income buys are poised to deliver the types of outstanding returns – and income streams – we’re used to. But I don’t expect these stocks and funds to remain cheap for long. The “eventually efficient” market will soon find its way to our portfolio, and bid up our names (providing those who own shares today with the 20%+ upside I mentioned).

So don’t miss my email update this Friday. It could be the difference between a comfortable retirement, and a destitute one. Click here to sign up for my 8% No Withdrawal Portfolio on a risk-free basis now.

Source: Contrarian Outlook