If you want to find the best high-yield opportunities on Wall Street, you don’t follow bright neon signs – you turn over rocks.

Years of research has shown that the most widely recommended names are typically overcrowded trades, killing any chance you have at wringing out any value.

Worse, analysts’ and pundits’ picks are often so conservative that they actually pose a danger to your retirement by producing sleepy returns and only so-so dividends.

That’s why I love closed-end funds (CEFs) like the three high yielders (between 7% and 9.5%) that I’m going to show you today.

They garner no media coverage, so they’re less likely to develop into bubbles.

And they provide the kind of dividends that will keep you comfortable well after you’ve said farewell to your job.

Just how underloved are closed-end funds?

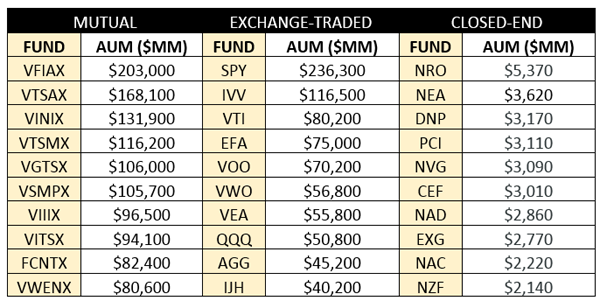

The following table shows the top 10 mutual funds, exchange-traded funds and closed-end funds by net asset values.

CEFs are small potatoes compared to their two more popular cousins:

CEFs: The Hidden Gems of Funds

Mutual funds, while losing their luster, have had decades to rack up tens and even hundreds of billions in AUM each, while ETFs have become the new hotness and command a few trillion dollars as a group.

CEFs? They go by mostly unnoticed. And that’s perfect for us income hounds.

Closed-end funds don’t get nearly the love of their exchange-traded brethren because they’re more expensive. But like you’ll typically notice when you dine out, you often get what you pay for. These actively managed funds expertly navigate several different assets and use leverage to provide investors with extremely juiced-up distributions.

Today, I want to show you three such CEFs that dole out yields between 7% and 9.5% … and somehow fly right under most investors’ radar.

Cohen & Steers Limited Duration Preferred and Income Fund (LDP)

Yield: 7%

Cohen & Steers has been expertly managing a variety of assets for more than three decades, and its Limited Duration Preferred and Income Fund (LDP) is a real gem. See, the mixed nature of LDP – it invests in preferred stocks, yes, but also other income-producing securities. That flexibility, in addition to its ability to use leverage, allows LDP to boast a 7% headline yield that puts it ahead of most straight-up preferred ETFs like the iShares U.S. Preferred Stock ETF (PFF).

The sector breakdown should feel familiar if you’re a preferreds lover, with nearly three quarters of the fund invested in financial stocks. And LDP is internationally diverse, with only half its assets dedicated to U.S.-based holdings, meaning its holdings include issues that range from Wells Fargo (WFC) to Japan’s Meiji Yasuda Life Insurance.

LDP is trading at a slight discount to its NAV right now – a welcome bonus! And monthly payouts make this perfect for retirees who intend on knocking out bills with investment income.

Nuveen AMT-Free Quality Municipal Income Fund (NEA)

Yield: 5.4%

Tax-Equivalent Yield: 8.9%

Municipal bonds help you stash more cash in your pockets and keep it out of the hands of the IRS, making them a favorite of serious income hunters.

You see, income from municipal bonds is tax-free at the federal level, and better still, you can also avoid state and local taxation if you reside where the bonds are issued. Thus, while the Nuveen AMT-Free Quality Municipal Income Fund (NEA) and its basket of about 1,000 municipal bonds sport a headline yield of “only” 5.4%, the so-called tax-equivalent yield – what a regularly taxed fund would have to yield to match NEA’s payout – is actually close to 9%.

NEA also is the perfect example of how ignored CEFs can get. Nuveen AMT-Free is one of the largest closed-end funds period at $3.6 billion in market cap – yet that would make it only the third-largest muni ETF, and it would sit behind a couple hundred other exchange-traded funds.

Somehow, I’m saying this about a fund that yields more than just about every other muni ETF … and trades at a 9% discount to boot! Their loss, our gain.

PIMCO Corporate & Income Opportunity Fund (PTY)

Yield: 9.5%

Last up is a staple of income portfolios – corporate debt. But like Cohen & Steers’ preferred fund, PIMCO Corporate & Income Opportunity Fund (PTY) doesn’t just delve in straight-up corporate debt – it can invest in agency mortgage-backed securities, municipals and even Treasuries.

PTY’s shareholders have laughed in the face of naysayers who were convinced that Federal Reserve rate hikes would spell doom for anything spinning off yield. Bond funds market-wide are enjoying a lift in 2017 – the SPDR Bloomberg Barclays High Yield Bond ETF (JNK) is up 2%, while the iShares 20+ Year Treasury Bond ETF (TLT) has gained 4%. But PTY is really putting together something special, roaring ahead by 15%!

And just a reminder: This is a bond fund.

Making things sickeningly sweet is the nearly 10% yield on PTY, delivered via a 13-cent monthly payout that has come like clockwork for years.

— Brett Owens

Live Off Dividends Forever With This “Ultimate” Retirement Portfolio [sponsor]

If you want to retire comfortably, you need big dividends. The steady drumbeat of income is what helps pays the bills and keeps you afloat when you’ve stopped collecting a paycheck.

But if you want to get through retirement without ever touching your nest egg, you need more than just giant dividends – you need dividend growth to beat back inflation, and you need capital appreciation to keep building your nest egg! Losers like WPG and IEP can’t do that … but the “triple threat” stocks in my 8%-yielding “No Withdrawal” retirement portfolio sure can!

How many times have you seen a pundit shill for OK-yielding blue chips like Coca-Cola or Kellogg? They’re not bad companies, but they leave you with just 3% to 4% in dividends, paltry payout hikes and little in the way of growth potential.

You and I both know that math doesn’t add up. Those 3% to 4% returns on a nest egg of half a million dollars will only generate $20,000 in annual income from dividends at the high end!

You’ve worked your tail off for decades. So you deserve more out of your retirement.

My “No Withdrawal” portfolio ensures that you won’t have to settle during the most important years of your life. I’ve put together an all-star portfolio that allows you to collect an 8% yield, while growing your nest egg – an important aspect of retirement investing that most other strategies leave out.

I’ve spent most of the past few months digging into the high-dividend world, and I’ve had to weed out several yield traps that looked great on their surface, but potentially disastrous at a closer look. The result is an “ultimate” dividend portfolio that provides you with …

- No-doubt 6%, 7% even 8% yields – and in a couple of cases, double-digit dividends!

- The potential for 7% to 15% in annual capital gains

- Robust dividend growth that will keep up with (and beat) inflation

This all-star cluster of stocks features the very best of several high-income assets, from preferred stocks to REITs to closed-end funds and more, that combine for a yield of more than 8%.

This portfolio will let you live off dividend income alone without ever touching your nest egg. That means never having to worry about how you’ll pay your monthly bills, and never having to worry about wrecking your retirement account if disaster strikes.

Don’t scrape by on meager blue-chip returns and Social Security checks. You’ve worked too hard to settle when it matters most. Instead, invest intelligently and collect big, dependable dividend checks that will let you see the world and live in comfort for the rest of your post-career life.

Let me show you the path to the retirement you deserve. Click here and I’ll provide you with THREE special reports that show you how to build this “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential – and it’s absolutely FREE!

Source: Contrarian Outlook