As with all types of stock market strategies, there are high-yield stocks that are undervalued gems and others that are time bombs in your portfolio. Often investors that are looking for a high dividend yield use stock selection criteria that are more appropriate for capital appreciation focused investment goals.

Using the wrong stock picking criteria will result in buying shares of high-yield stocks that are in a “death spiral” which will lead to the slashing of dividends and crashing of share prices.

[ad#Google Adsense 336×280-IA]The widely held investment belief is that high yield equals high risk.

Investors buy high-yield stocks with the hope that they can continue to earn that well above average yield.

The facts are that a high yield can be an indicator that the dividend is not sustainable. But that is not always the case.

A high yield stock may not be well understood by the market, and therefore the price is too low in relation to the safety of the dividend.

If your investment goal is to earn a high, but as safe as possible yield, you want to dig out the latter type of stock and avoid the first.

To avoid high yield stocks that end up crashing and burning in your portfolio, avoid these three investment strategies that may work for investors looking for share price gains, but are too risky for income-focused investors.

Don’t Buy Stocks for an Expected Turnaround. Buying shares of value stocks where the business is forecast to turn around can be a good investment approach for the investor who isn’t interested in dividends and is willing to wait several years to see if the stock can become a winner.

For the income stock, a turnaround play is a dividend suspension waiting to happen. If a company needs to make big changes to survive, the easiest way to start rebuilding is to stop paying the dividend and use that cash to pay down debt or rebuild the business. You want your dividend stocks to be companies that already are stable and growing their business.

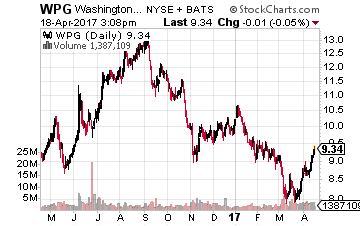

This means avoiding a stock like Washington Prime Group (NYSE:WPG) which yields over 11%.

This means avoiding a stock like Washington Prime Group (NYSE:WPG) which yields over 11%.

This REIT owns second tier shopping malls and is losing anchor tenants like Macy’s.

Some investors believe that the company can re-purpose empty space and recover lost rental income.

It’s not worth betting your dividend payments on.

Don’t Invest Because an Income Stock is in a “Sexy” Sector. Investors like to find stocks that might pertain to businesses involved in some new, disruptive technology. Look at the recent share price of Tesla Inc. (Nasdaq:TSLA). It now has a market cap larger than Ford or GM, even though Tesla’s revenues are a fraction of the old line car manufacturers’, and it continues to lose money by the barrel full.

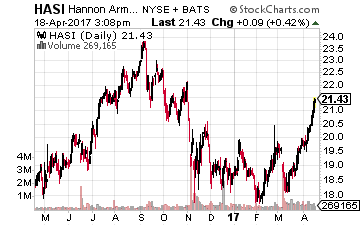

Hannon Armstrong Sustainable Infrastructure Capital (NYSE:HASI) is a REIT in the sexy renewable, sustainable energy space with an attractive 6.3% yield.

Hannon Armstrong Sustainable Infrastructure Capital (NYSE:HASI) is a REIT in the sexy renewable, sustainable energy space with an attractive 6.3% yield.

However, a deeper look shows that HASI is highly leveraged with very slim net income margins.

If its yield was over 10%, HASI might be a good value for high income investors.

At 6% this stock carries too much risk in relation to the cash yield.

Don’t Trust Management to Turn Things Around. The management teams of troubled companies always have good excuses about why they got into financial trouble in the first place. Not to mention grand plans and initiatives on how the company will recover from its current mess. Those plans may work out in the long run, but I always keep in mind that it was these managers that dug the current hole.

If a company is not earning enough cash to support the current dividend, but the management keeps promising they will get back to full coverage at some point in the future, just avoid the stock until that actually happens.

There is just as good or even better chance that management will be forced to slash the dividend after years and quarters of saying they would not.

There is just as good or even better chance that management will be forced to slash the dividend after years and quarters of saying they would not.

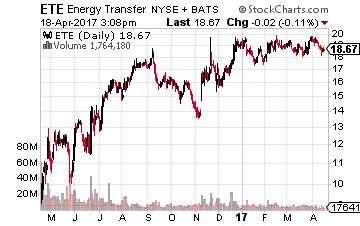

One to avoid is Energy Transfer Equity LP (NYSE:ETE) which only generated 57% of the cash to cover the 6% yield dividend.

Related company Energy Transfer Partners LP (NYSE:ETP) yields 12% but is only generating cash equal to 87% of the dividends.

ETE generates its cash flow from its ownership and distributions from ETP. This is a cash flow pyramid that could quickly collapse if the business does not improve.

— Tim Plaehn

Sponsored Link: Avoiding the wrong kind of high-yield stock is equally if not more important than investing in the right kinds. I have made my career by helping guide investors into the right kind of income stocks that are appropriate choices for developing an income stream that they can live on as well as helping avoid potential disasters in their portfolios.

After following my guidance for a couple of months I always get email from my subscribers saying that they have stopped worrying about the daily gyrations of the stock market. Instead, they earn consistent returns, paid in the form of cash. With the right guidance, it really is that easy. All you have to do is buy shares in the stocks that I recommend and watch as they deposit money into your brokerage account multiple times a month.

Right now, there are over 20 high-yield stocks available through my Monthly Dividend Paycheck Calendar, a system for generating a recurring monthly income stream from the market’s most stable high-yield stocks.

The Monthly Dividend Paycheck Calendar is set up to make sure you receive a minimum of 6 paychecks every month and in some months up to 14 paychecks from reliable high-yield stocks built to last a lifetime.

This unique tool will set you up to receive a more predictable dividend stock income stream that you can count on every month instead of just once a quarter like most other investors. Joining my calendar by Thursday, April 27th will give you the opportunity to claim an extra $1,791.70 in dividend payouts by May 17th.

The Calendar tells you when you need to own the stock, when to expect your next payout, and how much you can make from these low-risk, buy and hold stocks paying upwards of 12%, 13%, even 18%. I’ve done all the research and hard work, you just have to pick the stocks and how much you want to get paid.

The next critical date is Thursday, April 27th (it’s closer than you think), so you’ll want to take action before that date to make sure you don’t miss out. This time, we’re gearing up for an extra $1,791.70 in payouts by May 17th, but only if you’re on the list before April 27th. Click here to find out more about this unique, easy way of collecting monthly dividends.

Source: Investors Alley