Many people think a conservative, disciplined approach to retirement will help you reach your financial goals. They’re wrong.

If you invest too conservatively, you’ll never retire. At the same time, if you educate yourself about the financial options out there and invest accordingly, you can retire much, much earlier.

Let’s take a look at the math.

Higher Returns, Earlier Financial Freedom

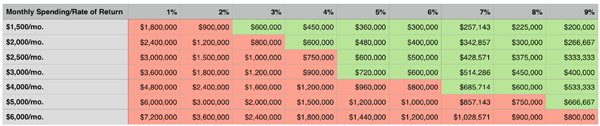

In the chart above, I’ve broken down how much money you need according to how much you spend per month and what rate of return you get on your investments.

In the chart above, I’ve broken down how much money you need according to how much you spend per month and what rate of return you get on your investments.

[ad#Google Adsense 336×280-IA]At one extreme, if you spend $1,500 per month and get a 9% annual rate of return, you need just $200,000 to retire.

At the other extreme, if you spend $6,000 per month and get just a 1% return, you need over $7 million.

Look at the difference between the numbers at the bottom right and the top left.

You can spend $6,000 a month and still retire on $800,000 or less if you get a 9% return, but you’ll still need well over $1 million, no matter how frugal you are, if you’re getting just 1%.

That sounds fine and good, but where can you get 9% annual returns, on average, over a long time horizon?

The answer is simple: the stock market.

The S&P 500 has offered an annualized return of more than 10% over the last 90 years. That’s including the stock market crash of 2008 and the Great Depression! Over the last 30 years, the index has offered a similar return—about 10% per year, despite downturns during three recessions:

Stock Returns Soar No Matter What

Invest $1,000 in the S&P 500, and 30 years later you’ll have over $25,000. That’s all you have to do: put $1,000 in the market. Invest $1,000 in the S&P 500 every year, and 30 years later you’ll have over $180,000.

Invest $1,000 in the S&P 500, and 30 years later you’ll have over $25,000. That’s all you have to do: put $1,000 in the market. Invest $1,000 in the S&P 500 every year, and 30 years later you’ll have over $180,000.

The stock market is a powerful tool to create wealth, which is why the wealthy love it and depend on it to make them wealthier.

Still, many middle-class Americans ignore the stock market and depend on their house as a wealth builder. How does that work in reality?

Not so well. If we look at the US House Price Index over the last 26 years (when the index started), we see that prices have gone up 140.2%, but stocks outperformed real estate eightfold.

Real Estate Is a Bad Bet

Of course, even more risk-averse investors will just put their money in a savings account and sleep well at night knowing they won’t lose it.

Of course, even more risk-averse investors will just put their money in a savings account and sleep well at night knowing they won’t lose it.

In reality, they should be having nightmares.

Here’s why: savings accounts are earning far less than 1% a year, but let’s give these investors the benefit of the doubt and assume savings accounts will start to offer 1% returns soon. Assuming that, how long would it take to retire?

The answer is simple and horrifying: more than 100 years.

A lot more, actually.

Impossible Retirement Goals

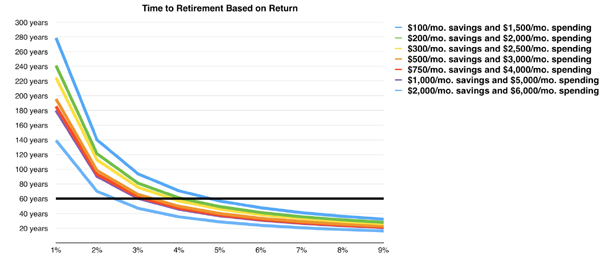

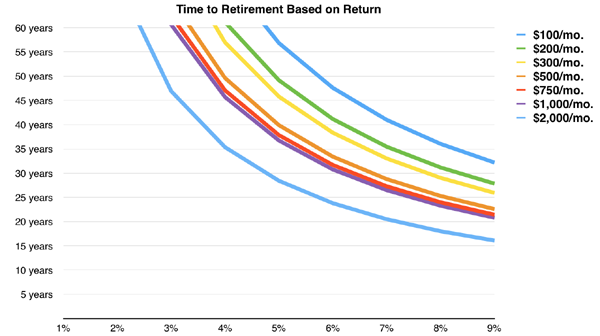

Ultra-conservative savings and retirement do not go hand in hand. The chart above shows us that you need to get at least a 3% return on your investments to reach retirement within a lifetime. Let’s zoom in on that part of the graph.

Ultra-conservative savings and retirement do not go hand in hand. The chart above shows us that you need to get at least a 3% return on your investments to reach retirement within a lifetime. Let’s zoom in on that part of the graph.

The Secret Behind a 9% Yearly Return

The big takeaway from this chart is that you will retire sooner if you can get a higher rate of return. With a 9% return, you can get there in less than 35 years—and the S&P 500 can get you there.

The big takeaway from this chart is that you will retire sooner if you can get a higher rate of return. With a 9% return, you can get there in less than 35 years—and the S&P 500 can get you there.

So how do you do it? The easiest way to get into the stock market is with an index fund. You can choose either exchange-traded funds (ETFs) or mutual funds. ETFs that track the S&P 500 include the SPDR S&P 500 ETF (SPY) and the Vanguard 500 ETF (VOO). The Vanguard Total Stock Market ETF (VTI) goes beyond the S&P 500, giving you even more diversification.

Index Funds Deliver Wealth

Another “set it and forget it” option is mutual funds. The three biggest and most popular S&P 500 funds are the Vanguard 500 Index Fund (VFINX), the Schwab S&P 500 Index Fund (SWPPX), and the Fidelity 500 Index Fund (FUSEX). Each of these have offered almost identical returns over the long term:

Another “set it and forget it” option is mutual funds. The three biggest and most popular S&P 500 funds are the Vanguard 500 Index Fund (VFINX), the Schwab S&P 500 Index Fund (SWPPX), and the Fidelity 500 Index Fund (FUSEX). Each of these have offered almost identical returns over the long term:

No-Drama Market Tracking

![]()

— Michael Foster

The Sweet Spot: 7%+ Yields and 12% to 38% Upside [sponsor]

Index funds are great tools, but if we want to live on dividends alone (and we should), without tapping our nest egg, their sub-2% yields just won’t cut it.

But luckily for us, thanks to some headline-driven insanity, there are once again corners of the market that pay dividend yields of 7.0% or better and boast 12% to 38% price upside, to boot!

This means you’ll easily be pulling in double-digit annual returns, with much of those gains coming in cash. These investments are safe, but they aren’t as well known as the S&P 500 ETFs and mutual funds I just showed you.

These stealth plays are the perfect investments for 2017, when one presidential tweet can rattle the markets. And once investors realize the crop of interest rate hikes the Fed’s planning this year will likely be disappointing, they’ll pile into these 7.0%+ payers and deliver us that nice 12% to 38% upside.

But you have to get in now, before their prices soar (and their yields shrink). Click here and I’ll share the names, tickers and buy prices on these bargain-priced dividend payers.

Source: Contrarian Outlook