I invest in the stock market to build a stable and growing dividend income stream. It is very difficult, if not impossible, to predict the direction of share prices. Most market direction forecasts are only useful for the short to intermediate term. I have developed stock buying, selling, and tracking strategies that help me towards the goal of a large and growing dividend income stream.

Here are a few strategies I use that may be out of step with what you have learned from the entertainment-focused financial news outlets.

Track your dividend earnings on a monthly or quarterly basis. The online brokerage account systems do a terrible job of tracking stock returns including dividends.

Track your dividend earnings on a monthly or quarterly basis. The online brokerage account systems do a terrible job of tracking stock returns including dividends.

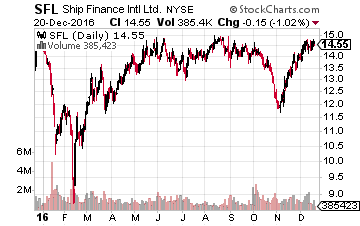

For example, I have accumulated shares of Ship Finance International Limited (NYSE: SFL) in one of my accounts. The brokerage account summary page shows the shares are up about 2.5%.

Yet with dividends included, the SFL shares have earned a 17% total return since I started buying into the stock. To know that information, I have kept a spreadsheet that lists each dividend stock I own, and the individual listings are updated with each share purchase and dividend earned.

Be willing to buy more shares of your income stock investments when the share price drops. This is a hard one for investors to do, but it will make a huge difference over years of investing. Again, using SFL as an example, my first purchase was at $16.07 per share. The current share price is $14.77, yet I am in a positive share value position in the stock.

[ad#Google Adsense 336×280-IA]That is because over the last two years I have made nine additional purchases at share prices ranging from $12.96 to $15.20.

When there is a significant short-term drop in the stock price, I look to buy more.

I also think about buying after a stock goes ex-dividend. Typically, the share price will drop by several percentage points as the “dividend capture” crowd rushes to sell after locking in the receipt of the dividend payment.

When you have cash available to invest, there is probably a stock or two in your portfolio, or on your stock wish list, that has dropped from recent highs.

These are the shares you want to think about buying and then consider which one fits into your overall portfolio strategy.

I have one or two stocks that I think of as “junk drawer” stocks. These are the very high-yield stocks that I can buy shares in when I find some extra cash in my brokerage account. Think of these stocks as a place where you can put some cash to work after you sell shares of one of your income stocks that have run up to a high price.

Yes, I like to take profits (usually a partial sale) if one of my income stocks is showing big gains compared to what I paid for the shares. Your junk drawer stock is also a place to put the proceeds back to work after one of your stocks unexpectedly cuts its dividend and you have to close out the position at a loss. It can happen to any of us.

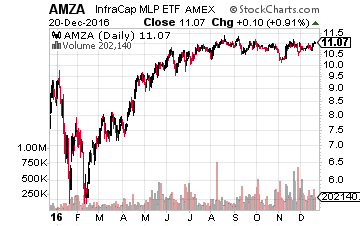

Your junk drawer stock needs to be one that pays a high yield and one where you have confidence in the underlying company value. In practice, this stock can turn extra cash into significant extra dividend income. Here is an 18% yielder from the Dividend Hunter recommendations list that I use as a stock to put extra cash to work to earn big dividends over time.

The InfraCap MLP ETF (NYSE: AMZA) is the first actively managed ETF in the MLP focused funds space.

The InfraCap MLP ETF (NYSE: AMZA) is the first actively managed ETF in the MLP focused funds space.

Here is how the InfraCap MLP ETF is designed to operate.

The fund owns the same MLPs as the ones tracked by the Alerian MLP Infrastructure Index, with the following possible enhancements to the index:

- The fund manager can weight individual MLPs holdings differently than the index. The AMZA is strictly market cap weighted, tracking the 25 largest midstream MLPs, with bigger MLPs having a greater weight on fund performance.

- AMZA will weight these same MLPs based on the return potential from the management team’s proprietary algorithm.

- The fund can own the publicly traded general partner companies of the index component MLPs. The general partner of an MLP can generate an accelerated level of cash flow growth compared to the limited partnership it manages. The GP companies can produce extra capital gains for the fund and a faster-growing distribution cash flow stream.

- The fund can sell call options (covered call strategy) to generate extra cash income from the portfolio.

- Fund managers can use a moderate amount of leverage (up to 33% of the portfolio). Leverage in an MLP fund helps offset a portion of the corporate income tax drag.

Recently, I contacted Ed Ryan, one of the portfolio managers, with a few questions about AMZA. It is good news to see that fund assets have grown tremendously this year, currently $135 million, compared to about $19 million at the start of 2016. The rapid growth in assets provides some challenges for the fund managers but is very good news for us investors for the long-term.

When I questioned the safety of the dividend, Ed stated that they currently do not think they will have to change the dividend rate since net capital gains (which have to be paid out at some point anyway) have been enough to support the current dividend.

Of more interest to me is the fund managers’ belief that MLPs are still greatly undervalued. They view the BBB bond yield as a benchmark for the midstream sector yield. That bond yield is now at about 4%, and midstream energy stocks are priced to yield an average of about 8%.

That spread is expected to narrow, and even if bond yields rise, MLP prices should also rise to help close the rate spread between the two asset classes. So even in a rising interest rate environment, MLPs and the AMZA share prices are poised to gain in value. In the meantime, we will continue to collect the 18% dividend yield the fund currently pays.

— Tim Plaehn

[ad#ia-tim]

Source: Investors Alley