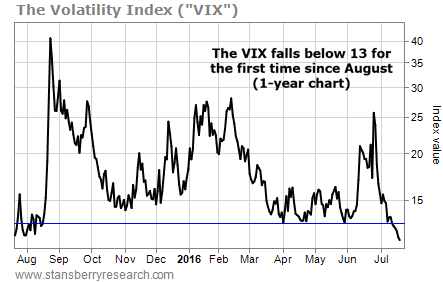

The market’s “fear gauge” just dropped to its lowest level in 11 months…

The last time it was this low was in August, just before the benchmark S&P 500 Index dropped 11% in six trading days.

[ad#Google Adsense 336×280-IA]This leads a lot of folks to believe investors are too complacent today… and that they’re about to get burned.

So today, we’ll look to history to see if they’re right. Our findings may surprise you… and help you earn larger trading profits in the months ahead.

Regular readers know the Volatility Index (“VIX”) is one of the most widely followed financial gauges in the world.

It’s also one of the most widely misunderstood.

The VIX is often called the market’s “fear gauge” because it measures the prices people are willing to pay for stock options…

When folks are worried about a crash, they buy put options to protect their portfolios against falling stocks… and put prices rise. The VIX rises with them. (The VIX can rise when folks go heavy on bullish bets by buying call options, too.)

When people are not worried about a crash, the VIX drops. As you can see in the chart below, the VIX just dropped to below 13 for the first time this year…

Over the past 25 years, the VIX has averaged a reading of 19.7. So we’re well below average now. People aren’t worried about a big crash in stocks.

But lots of traders take that information and assume it means that a big spike in volatility – and a big drop in stocks – is just around the corner. It doesn’t…

To test this, I looked at the S&P 500’s “drawdowns” after the VIX dropped below 13. A drawdown is the maximum loss for an asset or portfolio over a given period of time. For example, if you start the year with $100,000 and end the year with $100,000, but your account falls as low as $90,000 in that time, your drawdown would be 10%.

If a low VIX is usually followed by lower stock prices, you would expect to see bigger-than-normal drawdowns in the months after the VIX drops below 13. But that isn’t the case. In fact, it’s the opposite…

As you can see in the table below, the average one- and three-month drawdowns for the S&P 500 were smaller than normal after the VIX dropped below 13. The data go back to 1990.

Remember, drawdowns aren’t average returns. They are the worst returns at any point over the one- and three-month periods. And when the VIX dropped below 13 – as it recently did – the drawdowns going forward were smaller than during all periods.

In other words, the risk of a big drop in the coming months is smaller than it normally is.

You might ask, “But what about the big drop in August?”

That 11% drop was the largest one- or three-month drawdown, after the VIX fell below 13, since 1990. And there were 129 other instances. It was an anomaly.

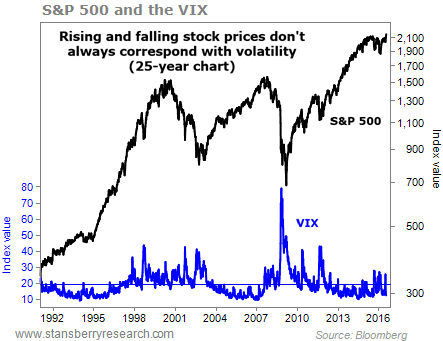

If you’re still not convinced, look at the chart below. It shows the S&P 500 (the black line) and the VIX (the blue line) over the last 25 years. You can see that stocks rose while volatility was below average from 1992 to 1997, 2003 to 2007, and for most of the time from 2012 to today.

Stocks can rise for years at a time while the VIX is below average. They can also rise when the VIX is above average. Look at the periods from 1998 to 2000 and 2009 to 2012.

A low VIX does not mean stocks are going to crash. There is no evidence to back up a statement like: “A low VIX means too much investor complacency and too little regard for risk, so a crash is around the corner.”

The VIX is low… And it’s a common discussion topic on the Internet and financial television. If you know the ideas we covered today, you’re ahead of 99.9% of your fellow investors.

Good trading,

Ben Morris

[ad#stansberry-ps]

Source: Growth Stock Wire