Want a diversified portfolio of uncorrelated assets with a big 8% yield? It’s possible, even in today’s overpriced market.

We can easily use just three funds to get a combined yield of 8%. That’s right—just three funds and we can turn $100,000 into a durable portfolio yielding over $660 in monthly income. These funds are in vastly different asset classes, and the dividends from one of them are even tax-free.

[ad#Google Adsense 336×280-IA]So what’s in this big income portfolio?

First, we have the Alerian MLP ETF (AMLP), which is still down from a year ago but has capital gains upside potential thanks to changes in how the market understands weak oil prices (more on this in a bit).

Then there’s the Nuveen AMT-Free Municipal Income Fund (NEA), a well-managed municipal bond fund that has avoided the Puerto Rico ugliness and seen its net asset value go up since inception.

Finally, we have nearly double-digit yields from the Pimco Dynamic Income Fund (PDI), a closed-end fund the market still fails to fully understand but has tremendous potential.

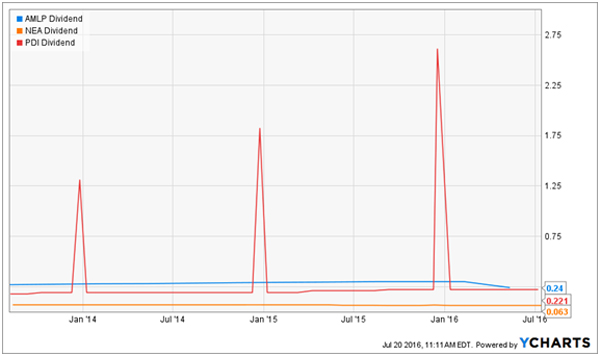

From a pricing standpoint, the portfolio is down 2% from a year ago, largely due to weakness in AMLP with the all-too familiar crash in oil, gas, and commodities:

Our High Yield Portfolio Has Traded Sideways

Meanwhile, the fund’s dividend cut has also worried investors:

Meanwhile, the fund’s dividend cut has also worried investors:

AMLP’s Recent Dividend Cut Concerned Investors

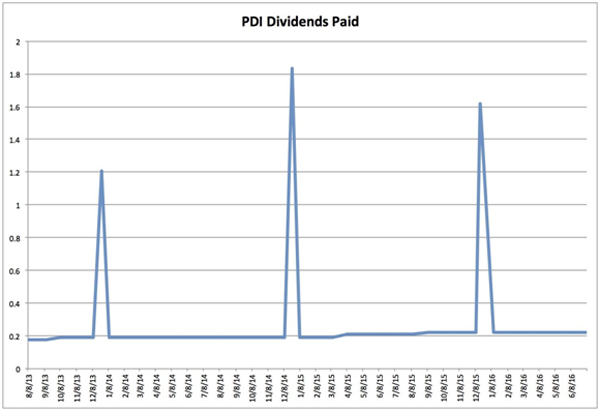

Fortunately for us, the special dividends from PDI handsomely offset this. Over the last three years, PDI’s special dividends have paid $4.67, a massive 16.9% income bonus above and beyond the 9.6% yield the fund currently offers:

Fortunately for us, the special dividends from PDI handsomely offset this. Over the last three years, PDI’s special dividends have paid $4.67, a massive 16.9% income bonus above and beyond the 9.6% yield the fund currently offers:

Massive Bonus Income

This more than offsets the recent decline in AMLP’s payouts, but a further decline is unlikely. This fund’s problem has been the fall in oil prices, which is now in the rear view mirror:

This more than offsets the recent decline in AMLP’s payouts, but a further decline is unlikely. This fund’s problem has been the fall in oil prices, which is now in the rear view mirror:

Oil’s Slide is Over – As is AMLP’s

I don’t see oil reaching its 2013 levels anytime soon, but I don’t see as dramatic a decline coming either. In fact, for the last year we’ve seen great volatility but still a limited range for oil prices: $25 is the floor, and $50 is the ceiling. This isn’t great for commodity producers, but it isn’t as bad as the free-fall we saw back in 2014. For this reason, AMLP’s weakness may be mostly a thing of the past, with limited downside left.

I don’t see oil reaching its 2013 levels anytime soon, but I don’t see as dramatic a decline coming either. In fact, for the last year we’ve seen great volatility but still a limited range for oil prices: $25 is the floor, and $50 is the ceiling. This isn’t great for commodity producers, but it isn’t as bad as the free-fall we saw back in 2014. For this reason, AMLP’s weakness may be mostly a thing of the past, with limited downside left.

Still, many investors feel burned. Anyone who held Kinder Morgan (KMI) or Boardwalk Pipeline (BWP) knows what weakness in the energy market can do to your income and your asset’s values. Both of these stocks slashed their dividends—Boardwalk cut by more than 80% back in 2014, and KMI cut by more than 75% earlier this year.

That second cut particularly angered investors, after several assurances from Wall Street and Kinder Morgan that a dividend cut was not in the cards turned out to be simply not true, and payouts were slashed. Of course, this was all the result of the disastrous fall in commodity prices, and now we are in a situation where commodities remain low, but still range bound.

Currently, AMLP isn’t priced for such a situation. Falling almost 30% in 3 years and nearly 16% in the last year, AMLP has only seen a bit of a recovery in 2016 (up 6.8%). It seems the market has just begun to realize it was too hasty in selling off MLPs, but remains still too squeamish to bring it back to a fair price. This makes it an ideal purchase right now, both for the high yield and for the potential of capital gains.

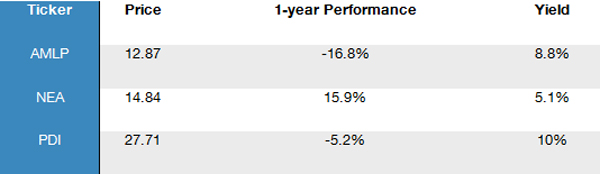

So what does our portfolio look like, when we put it all together? A bit like this:

Our 3-Fund High Yield Portfolio

An equal weighting to all three gets us a portfolio yielding 7.9%, just a hair under 8%. But remember those special dividends from PDI and the tax-free nature of NEA’s distributions, which will boost your effective yield much higher, depending on your tax bracket.

An equal weighting to all three gets us a portfolio yielding 7.9%, just a hair under 8%. But remember those special dividends from PDI and the tax-free nature of NEA’s distributions, which will boost your effective yield much higher, depending on your tax bracket.

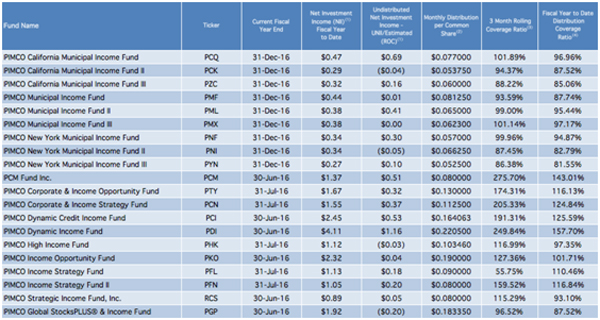

Ignoring taxation issues, PDI’s upcoming and still unannounced special dividend is likely to be as much as last year’s $1.62 cent payout, bringing our actual yield on this fund to over 15% and our average yield up to 9.8%. This is because PDI has better dividend coverage than any Pimco fund out there, with over $1 per share in undistributed net investment income just waiting to be released:

PDI Has an Extra $1 Per Share Waiting for Investors

At this point you must be asking yourself: How is PDI able to give such a monstrous income stream, and why isn’t everyone in it? The answer is quite simple: people don’t understand what this fund really does.

At this point you must be asking yourself: How is PDI able to give such a monstrous income stream, and why isn’t everyone in it? The answer is quite simple: people don’t understand what this fund really does.

Part of that is Pimco’s fault. The firm describes the fund mysteriously on its website:

“The fund normally invests worldwide in a portfolio of debt obligations and other income-producing securities of any type and credit quality, with varying maturities and related derivative instruments. The fund’s investment universe includes mortgage-backed securities, investment grade and high yield corporates, developed and emerging markets corporate and sovereign bonds, other income-producing securities and related derivative instruments.”

The corporate bond market has been hit hard in the last year by fears of rising defaults, while emerging market debt has been hurt by the fall in commodity prices. This was a double-whammy that caused PDI’s price to fall, but this sell-off makes no sense. When we look a little deeper, we see that a full 70% of PDI’s assets are in mortgage-backed securities (MBSs).

While the cause of the financial meltdown in 2008, nowadays MBSs have been incredibly strong. But memories of 2008 have kept a lot of people away from the asset class, causing these assets to remain underpriced despite falling default rates in the American mortgage market.

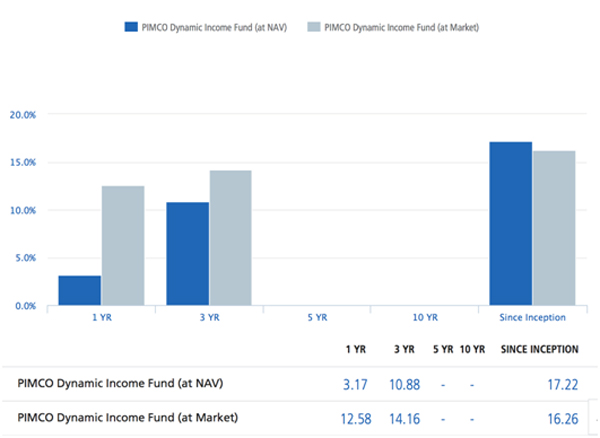

This has helped PDI earn a 17% annualized return on its NAV since its IPO three years ago:

PDI Earns a Gaudy 17% Annually Since Inception

This doesn’t mean we should dump all of our money in the fund. Of course, as 2008 reminds us, a financial meltdown can wipe asset values off quickly. Plus, PDI has an effective leverage rate of nearly 47%—very high, even for the CEF universe.

This doesn’t mean we should dump all of our money in the fund. Of course, as 2008 reminds us, a financial meltdown can wipe asset values off quickly. Plus, PDI has an effective leverage rate of nearly 47%—very high, even for the CEF universe.

At today’s extremely low interest rates, it makes sense for PDI to take advantage of cheap credit and extend its reach into the MBS market—a fact proven by its multi-year ability to far out-earn its distributions. But a quick change in the interest rate environment could change all that, so we need to limit our risk and diversify with a couple other funds.

A diversified approach with energy, municipal and residential mortgage exposure is a way to get massive yields while avoiding overpaying for equities as the S&P 500 continues to reach all-time highs. While this isn’t the only portfolio investors should hold, it’s a great option right now as we wait for stocks to correct from their sky-high levels.

— Brett Owens

Sponsored Link: If you want more ideas on how to create a diversified high-yield portfolio without overpaying for overbought stocks, there are more high quality dividend stocks and funds that are still underpriced with limited risk and great diversification. There are three funds that offer 8%, 8.4% and 11% annual dividends with up to 15% additional price upside. Click here and I’ll share with you [more information] and buy prices for these high-yield income investments.

Source: Contrarian Outlook