Bankruptcies in the oil industry have slowed down… But there are still huge pitfalls awaiting investors.

Take Whiting Petroleum (WLL), for example.

About two years ago, the Denver-based petroleum and natural gas exploration and production firm diluted its shares by 30% in a merger with rival Kodiak Oil and Gas.

And today, Whiting is destroying the value of its shares… again.

[ad#Google Adsense 336×280-IA]Back in July 2014, Whiting acquired Kodiak Oil and Gas for $6 billion.

It was a massive deal, centered on the Bakken Shale in North Dakota.

The deal made Whiting the new “King of the Bakken.” After the merger, it had 18 drill rigs operating, the most in that area.

It produced 107,300 barrels of oil per day there – 9% more than the other giant in the region, Continental Resources (CLR).

But the merger cost shareholders.

The company touted the deal as an “all stock” transaction, which meant it didn’t issue any debt. But what the company actually did was take on all of Kodiak’s debt.

Before the deal, Whiting had $2.75 billion in debt and 119 million shares outstanding. After the Kodiak deal, it had $5.6 billion in debt and 204 million shares outstanding.

That means the company issued 83 million new shares and doubled its debt.

The increase in shares is what’s most concerning. When a company issues new shares, they don’t magically appear out of nowhere. A company is like a pie. In order to cut more slices, each piece must be smaller.

That means at the time of the deal, every shareholder gave up 30% of the value of each share. So if your shares were worth $1 each, they were only worth $0.70 after the merger.

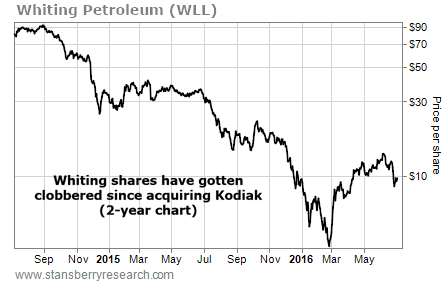

At the time, the company hoped the value of adding Kodiak would more than replace the lost share value. But as you can see from the chart below, that didn’t work out so well…

And it’s getting worse for Whiting investors today…

You see, there’s another deal coming that will add even more new shares to Whiting’s count… without adding any value.

Whiting needs to cut its $5.3 billion in debt. To do that, it has to offer its bondholders something in order to entice them to swap.

So… Whiting decided to offer them shares. Starting June 23, the company plans to convert $1.1 billion in bonds to new shares.

As long as Whiting’s share price remains above $8.75 – it closed at $9.66 last week – the company will convert 4% of the debt per day into new shares for 25 days. It’ll make the conversion at that day’s closing price.

That’s $43 million in new shares per day for about a month. The company has already converted nearly 30% of that debt into new shares.

In the worst-case scenario, Whiting will issue 122 million new shares.

That’s roughly 60% of the current share count, according to Bloomberg. In other words, existing shareholders will lose more than half the value of their shares as the company converts that debt. And remember, that’s after Whiting already diluted the value of shares by 30% in 2014.

That means Whiting shares will be worth about one-third of what they were prior to the Kodiak deal.

From the company’s point of view, this move is a better option than going bankrupt. For shareholders, it’s a huge loss.

This is a terrible situation. If you own Whiting shares, get out now.

Good investing,

Matt Badiali

[ad#stansberry-ps]

Source: Growth Stock Wire