It is hard to believe half of 2016 is almost in the books. Down here in steamy Miami, summer has been here for several weeks already. In the markets, the year is looking more and more like a repeat of 2015’s performance.

Thanks to an anemic global backdrop, weak domestic growth, and a strong dollar, the market is still locked in the same “profit recession” that commenced in last year’s second quarter.

[ad#Google Adsense 336×280-IA]Upcoming earnings reports should show the fifth straight quarter that earnings within the S&P 500 have declined on a year-over-year basis.

There are still pockets of value within equities, but they are few and far between.

I like the values and long-term prospects in biotech despite the deep bear market the sector has been in for almost a year now.

Homebuilders are cheap given the strength of the housing market and some of the lodging REITs look solid here with five to seven percent yields and discounts of 25% to 35% from their 52-week highs.

However, other than these sectors and a couple of one-offs I have profiled on these pages such as Ford (NYSE:F), General Motors (NYSE: GM) and Sequential Brands Group (NASDAQ: SQBG), I am not finding many standout values in the market right now.

In order to find some small and mid-caps I may have overlooked as attractive investments in this market, I am consulting the insiders. More specifically, I am looking at what insiders have actually purchased in recent weeks to uncover some additional values in equities. Here are three gems that insiders seem to like right now that just popped onto my radar.

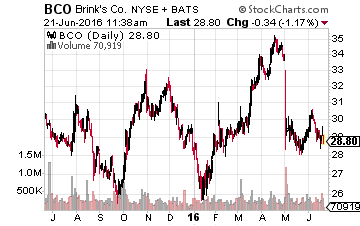

Let’s start with The Brink’s Company (NYSE: BCO), the well-known security and protection services firm whose name has been around for more than a century and whose armored trucks are ubiquitous on the streets of our cities.

Let’s start with The Brink’s Company (NYSE: BCO), the well-known security and protection services firm whose name has been around for more than a century and whose armored trucks are ubiquitous on the streets of our cities.

The company recently brought in a new CEO who promptly bought $2.5 million in new shares in early June. A week later another director bought over $200,000 in new stock.

Although the company did slightly miss expectations on its last quarterly earnings report, this is not a major turnaround effort. Earnings are increasing in the low teens on an annual basis. The stock is selling for under 14 times next year’s profit consensus, a discount to the overall market multiple. It is even cheaper on a free cash flow basis where its sports better than a 10% free cash flow yield. The stock pays a small dividend of 1.4%.

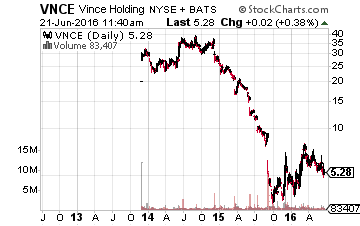

Next up we have retail play Vince Holding Corp. (NYSE: VNCE).

Next up we have retail play Vince Holding Corp. (NYSE: VNCE).

As can be seen above, this company is the walking embodiment of what I call a “Busted IPO” as the stock is selling for nickels on the dollar from where it came public in late 2013.

Vince was established in 2002 and offers a wide range of women’s, men’s, and children’s apparel, women’s and men’s footwear, and handbags.

Vince products are sold and distributed worldwide, including over 2,500 distribution locations across 42 countries. Based in New York and with its design studio in Los Angeles, the Company operates 32 full-price retail stores, 12 outlet stores, and its e-commerce site.

Revenues fell more than 10% in its FY2016 that ended in January. This year, sales growth should be flat and the company should do just better than break even as far as earnings. Next year, the company should return to solid profitability on revenue growth in high single digits according to the current analyst consensus.

Insiders seem to be buying into this turnaround scenario. Three directors have purchased over $1.2 million in shares with purchases in April, May, and June. Beneficial owners have made even larger purchases over that time period. The company has a solid balance sheet and is selling at a very cheap price to sales ratio compared to competitors.

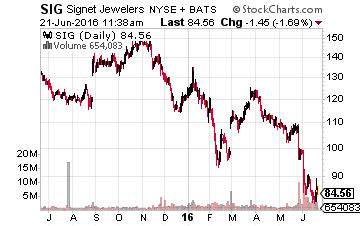

Another retailer is turning up on top insider buying lists recently as well.

Another retailer is turning up on top insider buying lists recently as well.

It is Signet Jewelers (NYSE: SIG) known for brands like Kay, Zales, and Jared.

The stock is down some 40% in recent months due to accusations around “diamond swapping” and the overall weak environment for retail so far here in 2016.

Insiders are signaling this recent dip is a buying opportunity with their recent purchases. Approximately 10 insiders have purchased more than $1 million in collective shares so far in June. The current consensus has earnings growing 30% or better both in FY2016 and FY2017.

Merrill Lynch and Nomura Holdings have also reiterated Buy ratings with price targets 40% to 50% above Signet’s current stock price over the past couple of weeks. Given the shares sell at 10 times this year’s projected earnings, it certainly seems a lot of bad news is already priced into the stock and they represent good value in the current market.

— Bret Jensen

[ad#ia-bret]

Source: Investors Alley

Positions: Long F, GM, and SQBG