Many investors are drawn to high-yield stocks. Being paid 10%, 12%, or even 15% on your investment in cash dividends seems a more certain and predictable approach to earning attractive returns compared to trying to predict the downs and ups of non-dividend or low-yield stocks.

This strategy can work until the company behind a high-yield stock slashes its dividend rate. This event will cause the double whammy of lost future income and usually lost principal value as the share price also gets hammered by the market.

[ad#Google Adsense 336×280-IA]My stock market research is focused on dividend stocks, and I do think that a well selected portfolio of high-yield stocks can provide both an attractive cash flow income stream and reasonable portfolio value protection over time.

The challenge is to be able to separate those high-yield companies that can continue to support and possibly grow their dividend payments vs. those that will eventually be forced to cut the payouts to investors.

One investing maxim is that a very high yield is a sign that the dividend rate is unsustainable.

That is not always the case, but if you buy into stocks that have yields in the teens, you need to understand if the company is generating enough cash from their business to continue paying the dividend.

My analysis of companies that pay a high yield involves researching and forecasting the free cash flow per share a company is generating. It is a task that requires continuous monitoring of the quarterly earnings reports to determine if cash flow is stable, growing, or declining.

A different analysis approach is required to dig out distributable cash flow per share, and the topic is a popular one when I am invited to present my strategies at various investor conferences.

The biggest goal of cash flow analysis is to find those high-yield stocks that are in danger of a dividend reduction and either not buy them or sell them if you already own shares. Here are five that need to be sold immediately and one example of a stock I recommend with a safe double-digit yield.

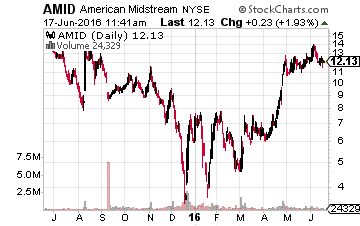

American Midstream Partners LP (NYSE:AMID) is a master limited partnership (MLP) whose business involves gathering, treating, processing, and transporting natural gas in the Gulf Coast and Southeast regions of the United States.

American Midstream Partners LP (NYSE:AMID) is a master limited partnership (MLP) whose business involves gathering, treating, processing, and transporting natural gas in the Gulf Coast and Southeast regions of the United States.

Due to the bear market in energy commodity prices, many MLPs have been forced to slash their distributions.

In April AMID reduced its quarterly distribution by 13%. Unfortunately, distributable cash flow is still just 75% of the new lower distribution rate. This MLP needs to cut another 25% to 30% out of its payments to investors. That attractive 13.8% yield is not safe.

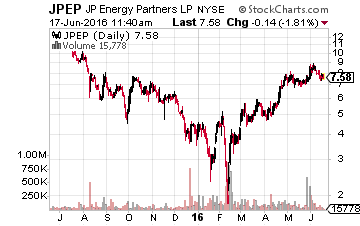

JP Energy Partners LP (NYSE:JPEP) is an MLP that owns and operates crude oil pipelines and storage, crude oil supply and logistics, refined products terminals and storage, and NGL distribution and sales.

JP Energy Partners LP (NYSE:JPEP) is an MLP that owns and operates crude oil pipelines and storage, crude oil supply and logistics, refined products terminals and storage, and NGL distribution and sales.

JPEP currently yields 17%.

The partnership has paid a level $0.325 quarterly distribution since going public in late 2014.

Over the last year, distributable cash flow was just 79% of the distributions paid. In the current energy price environment, MLPs on the edge of having enough cash to cover their payments are cutting distributions to ensure their financial stability in an uncertain market. It is likely that JPEP will significantly reduce the quarterly payout to preserve more of its cash flow.

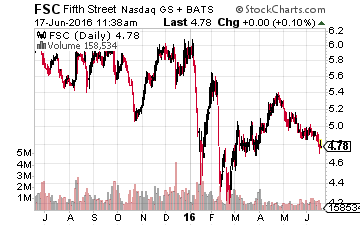

Fifth Street Finance Corp. (NASDAQ:FSC) is a business development company (BDC) that currently yields 15.1%.

Fifth Street Finance Corp. (NASDAQ:FSC) is a business development company (BDC) that currently yields 15.1%.

FSC’s total income from its loan portfolio has declined for six consecutive quarters.

In the 2016 first quarter, net investment income per share dropped below the $0.18 quarterly dividend rate.

This is a BDC whose business is on a downward trajectory, and under the BDC rules it is very difficult to turn a company’s fortunes around without cutting the dividend.

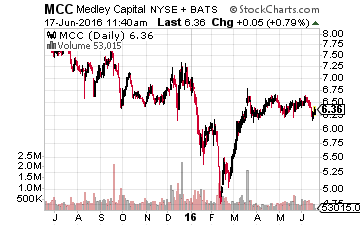

Medley Capital Corp (NYSE:MCC) with its 19% yield is another BDC that is not earning its dividend in net investment income per share.

Medley Capital Corp (NYSE:MCC) with its 19% yield is another BDC that is not earning its dividend in net investment income per share.

MCC’s problem is that about 6% of its loan portfolio is in non-accrual status, meaning those loans are not paying interest and could lead to principal value write downs.

For the first quarter, MCC reported net investment income of $0.26 per share and declared a $0.30 per share dividend. This dividend rate is under strong pressure to be reduced.

Orchid Island Capital Inc. (NYSE:ORC) is a finance REIT that owns a highly leveraged portfolio of government agency guaranteed mortgage backed securities (MBS).

Orchid Island Capital Inc. (NYSE:ORC) is a finance REIT that owns a highly leveraged portfolio of government agency guaranteed mortgage backed securities (MBS).

This business model generates cash flow to pay high dividends based on the interest rate spread between the MBS and the short-term cost to borrow money to finance the portfolio holdings.

Over the last year, the yield curve has flattened significantly squeezing the spread Orchid Island and other agency mREITs can earn. Several of ORC’s peers have already reduced their dividend rate. In the 2016 first quarter, Orchid Island earned enough net income to cover the dividend, but the rate spread decrease will eventually catch up and the dividend rate will be reduced. ORC currently yields 16%.\

A high yield is not always an indicator of a pending dividend reduction. Sometimes, for a variety of reasons, the market just gets it wrong. Here are a few high yield stocks in the same sectors that are not in danger of cutting their payouts.

Enbridge Energy Partners, LP (NYSE:EEP) is a strong, large-cap pipeline MLP that currently yields 10.6%.

Hercules Capital Inc (NYSE:HTGC) is a BDC with a long and steady history of dividend payments and occasional dividend increases. The stock yields 10.2%.

New Residential Investment Corp (NYSE:NRZ) is a finance REIT that does not depend on the yield curve and piles of leverage to generate its revenues. NRZ is more than likely to soon announce a dividend increase. The stock yields 13.6%.

Finding stable companies that regularly increase their dividends and avoiding stocks about to cut their dividends is the strategy that I use myself to produce superior results, no matter if the market moves up or down in the shorter term. The combination of a high yield and regular dividend growth is what has given me the most consistent gains out of any strategy that I have tried over my decades-long investing career.

— Tim Plaehn

[ad#wyatt-generic]

Source: Investors Alley