It was fun while it lasted.

I’m talking about the brief buying opportunity last winter, when the S&P 500 plunged 10% in the first six weeks of 2016.

On February 10, the day before the market hit its midwinter trough, I bet that it was ready for a turnaround, as the number of bearish option bets had hit a 10-year high—a clear contrarian indicator.

[ad#Google Adsense 336×280-IA]I then gave you the names of three stocks to buy straightaway.

As if on cue, all three went on to clobber the index’s subsequent 13.3% rise: Ventas Inc. (VTR) exploded for a 33% gain, while HCP Inc. (HCP) soared 22%. The Vanguard REIT Index Fund (VNQ), took off on a 15.5% run.

But now, with the market back above where it was at the start of the year—and trading at a nosebleed 24 times trailing-twelve-month earnings—deals like these are getting scarce.

One place you can still find them is overseas, particularly the three cheap dividend growers I told you about [recently]. But don’t write off the U.S. just yet, because even in an overpriced market, there are always top-quality names that aren’t getting their due from investors.

How do you find them? Start with the simple guideline Benjamin Graham, the father of value investing, gave us: look for stocks trading at or below 15-times earnings and 1.5-times book value. Here are three that would certainly be on Graham’s radar now.

An Insurer Ben Graham Would Love

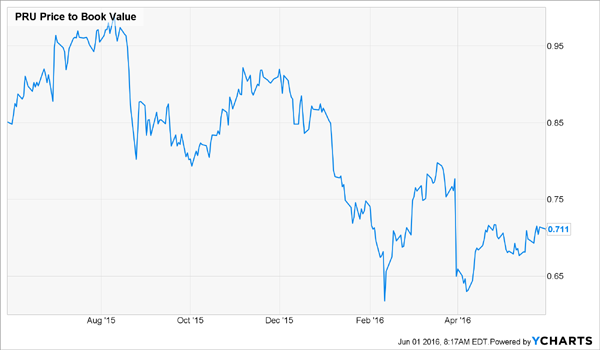

To say Prudential Financial (PRU) is cheap would be a huge understatement. The stock trades at just 71% of book value and 8.3-times forward earnings, ridiculously low levels for a company that generated $14.7 billion in free cash flow (FCF) in the last 12 months. That’s 42% of PRU’s $35-billion market cap!

The 141-year-old firm is still atoning, in investors’ eyes, for its 2013 dividend cut. As part of its penance, management has boosted the payout by 75% since then.

And if that’s not enough to get PRU back into the herd’s good books, there’s plenty of room for more: the company has paid out $1.17 billion in dividends in the last 12 months, or just 8% of FCF. That’s a far cry from the 147% it was paying out just before the 2013 cut.

Wall Street expects Prudential’s earnings to move more or less sideways over the next couple years, but its focus on retirement solutions will serve it well in the long haul as more baby boomers punch out, with 10,000 turning 65 every day.

Besides, with a 3.6% dividend yield and quarterly payouts rising fast, shareholders won’t need much near-term pop in the stock price to reap a nice profit.

A Bargain Food Stock With 14% Upside

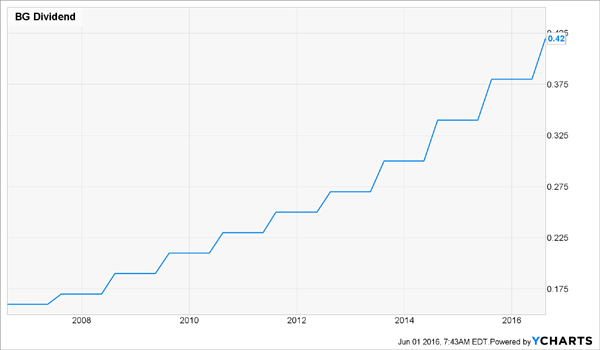

New York–based Bunge (BG) is another Ben Graham–friendly stock that’s a great buy now, trading at just 11 times forward earnings (a 14% discount to the five-year average) and 1.5-times book value.

Management certainly sees it that way: over the first four months of the year, it jumped on a dip in the share price to buy back $200 million worth of stock, cutting the total outstanding by more than 2%.

The 198-year-old company ships, stores and processes crops; makes margarine, mayonnaise and other products for the foodservice industry; produces ethanol and other biofuels; and sells fertilizer.

Margins tend to be thin at Bunge’s commodities-trading and crop-handling operations, so management aims to churn out more (and more profitable) refined products. Case in point: its just-announced decision to buy 63% of European edible oil and fat supplier Walter Rau Neusser, which is a perfect fit with Bunge’s existing ingredients business.

The stock yields 2.5% today, just a bit above the S&P 500 average, but the payout’s been growing like a weed—16% a year, on average, over the past decade. With just 33% of earnings going out the door as dividends and a global population that’s only getting bigger—and hungrier—you can bet on those hikes continuing.

This Cheap Dividend’s Moving on Up

Looking for one-click exposure to the entire real estate market? Brookfield Property Partners (BPY) is about as close as you can get. The company owns office buildings, shopping malls, hotels, industrial properties and apartment buildings across four continents, including high-demand cities like London and New York.

It’s a 250-million-square foot behemoth that’s throwing off steady funds from operations (FFO), more than 80% of which management sends out to investors in the form of a dividend that yields a gaudy 4.7%.

The company has only traded publicly since 2013, when it was spun off from Brookfield Asset Management (BAM), and it’s worked in two dividend hikes in the last year and a half, for a combined 12% increase.

In all, Brookfield is shooting for annual total returns of 12% to 15%, and it’s already coming in at the high end, delivering a tidy 14% in 2015.

The best is yet to come, thanks to BPY’s strong lease-renewal rate and management’s acquisition savvy: last month, it snapped up 5,700 modern student-housing units in the U.K.—where there are currently 2.1 students for every bed available.

The best part? With the units trading at 16% below book value, you can grab a piece of the action for just $0.84 on the dollar. That’s a deal Mr. Graham would sign off on in a heartbeat.

— Brett Owens

Turn a 4.7% Yield Into an 11% Income Powerhouse Instantly [sponsor]

I’m sure you’ll agree that a 4.7% yielder trading at 16% below book is a rare find these days. But what if I told you that you could double that yield with three other screaming bargains I’m pounding the table on right now?

They’re an often-ignored asset class called closed-end funds, and today my three favorites are delivering their shareholders safe payouts of 8.0%, 8.4% and 11.0%. And unlike Brookfield, they drop those fat “paychecks” into your investment account monthly.

But here’s one thing they do have in common with the real estate juggernaut: they trade at big discounts to the value of their assets—I’m talking markdowns of 7% to 15%—so you’ll catch a nice ride up in the share price as that gap shrinks.

Don’t wait. Click here to get [more information on] these “slam-dunk” income plays and start your new monthly income stream now.

Source: Contrarian Outlook