Usually when you find a company that has raised its dividend every year for 16 years, has never cut the dividend and, in fact, has lifted the payout to shareholders in 52 of the past 64 quarters, that dividend is considered safe.

But these days in the energy sector, you can’t assume “usually” still works.

Anyone who has paid the slightest attention to the markets and economy knows that the price of oil has plummeted over the past year. And that has affected nearly every company in the sector.

[ad#Google Adsense 336×280-IA]Midstream MLPs were supposed to be relatively immune. “Midstream” refers to the fact that these companies don’t drill for oil, nor do they refine it.

They simply transfer oil and gas from point A to point B.

Theoretically, they do not feel the impact of commodity prices because they get paid fees for transporting the oil and gas.

They are essentially toll takers.

But that hasn’t exactly been the case for many MLPs.

Their stock prices and distributions (MLPs pay distributions, not dividends) have gotten walloped like everything else in the sector.

Let’s drill into the numbers for Plains All American Pipeline (NYSE: PAA) – an oil pipeline and transportation MLP with a nearly 13% yield and the exceptional distribution-raising track record mentioned above.

It should be noted first that despite the carnage in the oil patch, Plains All American raised the distribution every quarter in 2015. In the first quarter of 2016, it kept the distribution the same at $0.70.

The best way to measure an MLP’s ability to pay its distribution is by looking at distributable cash flow.

In 2015, Plains All American generated $1.47 billion in DCF. It paid out $1.71 billion in distributions. So it did not generate enough cash flow to pay its distribution. In fact, the company’s cash flow was only $0.86 per dollar that it paid out.

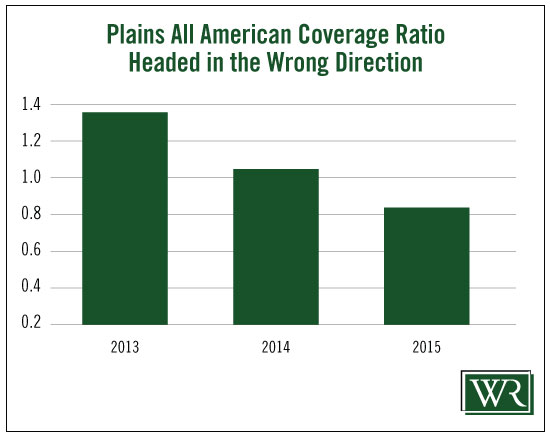

That ratio of cash flow to distributions paid is called the coverage ratio, and you always want it to be above 1. A coverage ratio above 1 means the company’s cash flow is higher than the distribution. In 2015, Plains All American’s coverage ratio was 0.86.

That wasn’t always the case. In 2014, the coverage ratio was 1.07. And in 2013, it was 1.37.

So not only is the coverage ratio going the wrong way, but it also is below 1, which is a problem. That means the company is funding the distribution from some other method besides running its business. The additional needed cash could come from cash in the bank, debt financing, sale of stock, etc.

So not only is the coverage ratio going the wrong way, but it also is below 1, which is a problem. That means the company is funding the distribution from some other method besides running its business. The additional needed cash could come from cash in the bank, debt financing, sale of stock, etc.

Management said, long term, it expects to grow the coverage ratio back to the 1.05 to 1.1 level.

That would make me feel much more secure about the distribution.

But that probably won’t be this year. In 2016, DCF is projected to fall to $989 million.

But that probably won’t be this year. In 2016, DCF is projected to fall to $989 million.

That will not come close to covering the distribution.

That will be two years in a row in which the company had to fund the distribution to shareholders by some means other than the cash generated from running its business.

Perhaps in 2017, the company will get back on track.

But for now, with shrinking cash flow that is not expected to cover the distribution, the distribution has to be considered vulnerable to a cut.

Dividend Safety Rating: F

Good investing,

Marc

[ad#sa-income]

Source: Wealthy Retirement