It’s a question I get a lot, both from members of my Contrarian Income Report service and folks who drop by our ContrarianOutlook website:

How do you invest your own nest egg?

I’ll answer it in just a moment.

[ad#Google Adsense 336×280-IA]I was reminded of this question again last week, when I was looking at the returns of the Vanguard Dividend Appreciation ETF (VIG)—and thinking about how dead simple it would be to beat the fund’s return over the long haul.

All it would take is the slightest bit of research.

Big on Hype, Short on Performance

VIG is one of the best cases I’ve seen of an investment taking an inherent advantage and getting nothing out of it.

The fund tracks the NASDAQ US Dividend Achievers Select Index, which includes 184 companies that have raised their payouts annually for at least 10 years. For that reason, it gets a lot of airtime from the pundits, who regularly peg it as a proxy for dividend growers in general.

And if you’ve read my columns, you know I’m a big fan of dividend-growth stocks.

The reason: they consistently rack up some of the market’s biggest gains.

What I consider the leading study on the subject, by research firm Ned Davis & Associates, proves it. After sifting through 43 years’ worth of data, from January 1972 through December 2014, Davis’s researchers found that dividend growers topped all other types of stocks.

It wasn’t even close: with a 10.1% average annual return, they blew away steady payers (7.1%) and non-payers (2.6%).

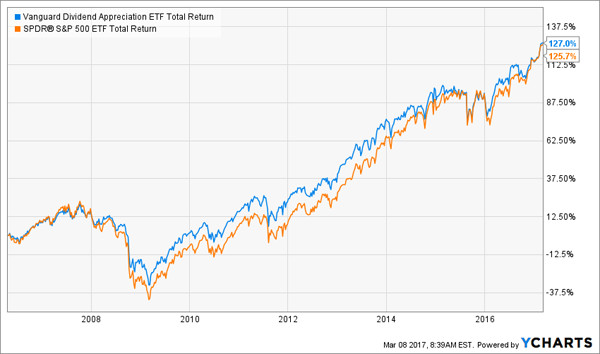

So VIG should easily beat the S&P 500, then, right?

Wrong.

Stretch it over any timeframe: one year, three years, five years, 10 years and since VIG’s inception in 2006, and at best your return would have just barely squeaked past the market’s.

Dividend-Growth Edge Goes AWOL

That’s disappointing, given VIG’s built-in edge.

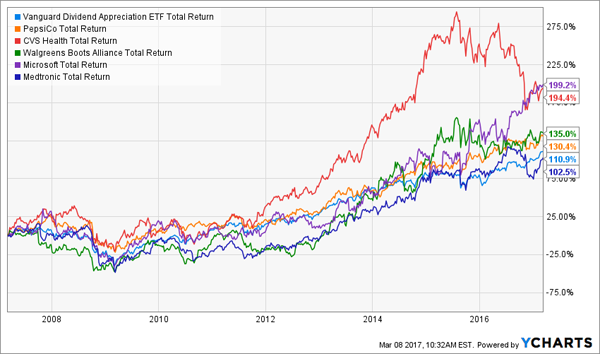

Now let’s go one step further and pick the five fastest dividend growers among VIG’s top 10 current holdings (without even getting into P/E ratios, earnings history, revenue growth and the like) over the past decade.

Those five stocks are CVS Health (CVS), Walgreens Boots Alliance (WBA), Microsoft (MSFT), PepsiCo (PEP) and Medtronic (MDT).

A quick backtest shows that all but one (Medtronic) have outperformed VIG:

Active Investing Wins Again

Holding these five would have handed you a 152.3% total return, compared to 110.9% for VIG, as their relentless dividend growth (ranging from 150.8% for PepsiCo to a massive 733.3% for CVS) squeezed their share prices higher.

And that’s just the result of a fairly “dumb” dividend-growth strategy. Now let’s see what happens when we add just a little more refinement.

Which brings me to…

Where My Retirement Cash Is Going Now

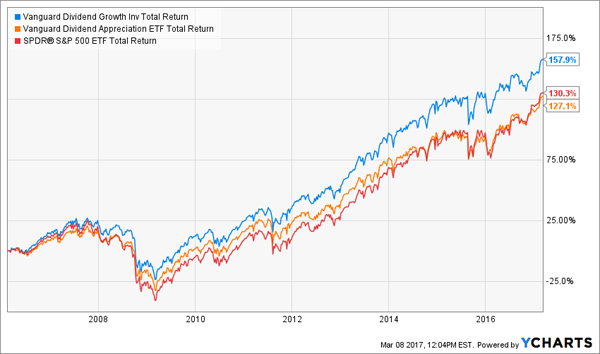

Right now, I’m putting 100% of my 401(k) contributions into VIG’s cousin, the Vanguard Dividend Growth Fund (VDIGX). That’s because I have to choose from a set list of funds, but at least one of them is VDIGX, which is a proven winner.

According to the prospectus, VDIGX focuses on “high-quality companies that have prospects for long-term total returns as a result of their ability to grow earnings and their willingness to increase dividends over time.”

Manager Donald J. Kilbride also considers factors like valuation and future dividend-growth potential. That’s a much more focused approach than VIG’s.

Kilbride’s stewardship comes at a cost, however: the fund’s expense ratio is 0.33%, more than three times higher than VIG’s 0.09%. But he’s earning his keep, delivering a total return that’s crushed VIG and the market since VDIGX’s inception in February 2006 (net of fees, of course):

The Power of a Focused Dividend-Growth Strategy

But if you’re thinking of buying VDIGX now, you’re out of luck. Vanguard closed the fund to new investors in July 2016.

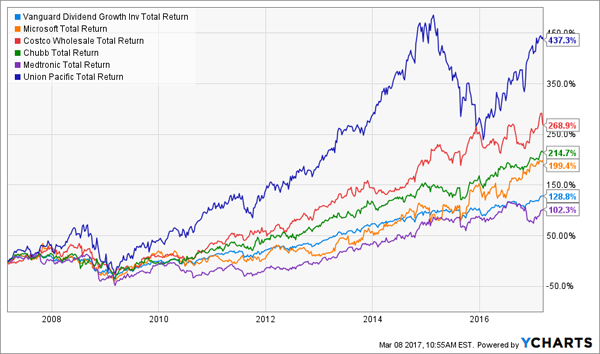

Even so, as with VIG, we can do an end run around that and pick the five fastest dividend growers (again over the past 10 years) from among VDIGX’s top 10 holdings, which combined make up 29.8% of the portfolio.

Here, we’re getting both fast dividend growth and piggybacking on Kilbride’s eye for value and dividend-growth potential.

These stocks are: Microsoft (MSFT), Costco Wholesale (COST), Chubb (CB), Medtronic (MDT) and Union Pacific (UNP). (For this back test, I’ve left out Canadian National Railway (CNI), whose dividend growth would have qualified it in Canadian-dollar terms but falls short when converted to US funds.)

Again, we see the same result: four of these five beat VDIGX, with the sole exception, again, being Medtronic:

Active Investing: 2, Passive: 0

What’s more, these five dividend growers generated a combined total return of 244.5%. That’s far more than the 152.3% we squeezed out of our five VIG selections.

It also neatly captures the power of combining dividend growth with bargain valuations, a strong earnings history and other signs of payout strength.

The bottom line? Investing in a “dumb” dividend-growth ETF is okay. A “smart” one is better, and picking your own dividend growers (which, by the way, is how I invest my personal retirement stash) is hands-down the best way to go.

— Brett Owens

The Sweet Spot: 8% Yields With Dividend Growth [sponsor]

Dividend growth is great, but none of the stocks above yield more than 2.8% today. What if you need big dividend income now so you can retire comfortably?

After all, 2.8% just won’t cut it unless you’re rich already!

But you can retire on as little as $500,000 today by focusing on stealth income plays such as closed-end funds (CEFs), preferred shares and real estate investment trusts (REITs). In many cases, these issues pay secure yields of 8% or better—with dividend growth to boot!

This means you’re assuring yourself of 10%+ annual returns, with most of that coming as cash dividends! These vehicles are safe, but they aren’t as well known as your typical (and usually expensive) blue chip. And that’s good for us, because we can lock up secure income streams of 8% or more while enjoying payout growth and price upside, too.

The 6 bargain buys I want to show you today are perfect for 2017. Because no matter what happens in Washington or with the Fed, these 8% payers are going to become increasingly popular with retirees as they’re discovered. Make sure you buy them now, before their prices get bid up (and their yields get squeezed). Click here for full details on my favorite 8% plays in funds, preferreds and REITs—and I’ll share the names, tickers and buy prices with you, too.

Source: Contrarian Outlook