The stock market’s up, which means yields are down. And while there are still some generous payers available, be careful – entire sectors are paper tigers that will probably suffer this year.

[ad#Google Adsense 336×280-IA]Two weeks ago, we discussed the best 7%+ dividends for 2017. Today we’ll talk about the big dividends that should be avoided, or sold altogether.

Mortgage REITs (mREITs) for starters tend to drop their dividends over time – and these cuts accelerate when rates rise. Profits plummet because their portfolios (typically made up of fixed-rate issues) decline in value as rates run higher.

We’ve discussed the benefits of buying dividend growth at length. Why would you ever want to do the opposite and purchase these “falling payout knives”?

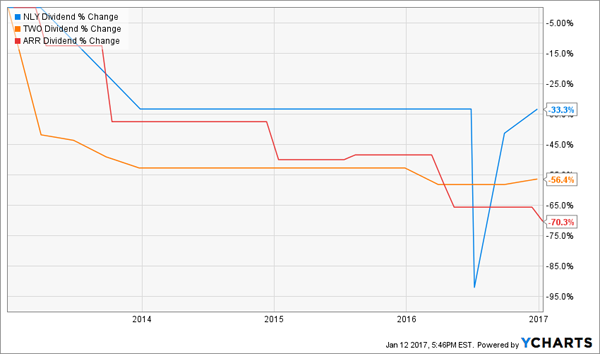

mREIT Dividends Race to the Bottom

Granted, the current yields of Annaly Capital (NLY), Two Harbors (TWO) and ARMOUR Residential (ARR) all look great (above 10%) on paper. But those payouts are living on borrowed time and their share prices will suffer as dividend cuts are made.

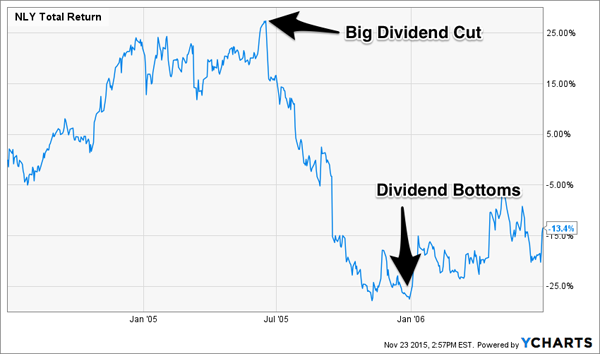

Now some delusionally bullish hopefuls may argue that the prospect of rising rates is already priced into mREIT shares. But history shows that isn’t usually the case.

Despite the stock market’s reputation as a “forward-looking vehicle” Mr. Market didn’t price anything into Annaly shares until it actually cut its dividend by 20% during the last rising rate period (June 2005). Share prices bottomed exactly when the dividend bottomed at $0.10 per share (down from $0.50 a year earlier) in December 2005.

Mr. Market Didn’t Look Ahead With Annaly

Business development companies (BDCs) are often lumped with mREITs. And there are some similarities in that both vehicles tend to:

- Boast big current yields,

- Pay most of their income to investors, and

- Cut their dividends without thinking twice!

BDCs have a bit more flexibility when it comes to dealing with higher rates, however. Their profits, which come from loans they make to small businesses, can rise as rates increase.

But the trick to timing your BDC purchases doesn’t involve any rate forecasting. You should simply buy them when they are trading well below book value, as I pointed out in December 2015. Since that time, the three most promising firms – Prospect Capital (PSEC), Ares Capital (ARCC) and Main Street Capital (MAIN) – have rallied 18% to 34%:

Big Returns From BDCs…

But all of these gains were driven by investors willing to pay higher price-to-book ratios!

… All Thanks to Book Value Premiums

The big discounts offered a year earlier have been snapped up. And you’re better off waiting for them to return, as they always do, rather than chasing these stocks higher.

Let’s revisit PSEC, for example. It’s returned 121% to investors since its 2004 IPO – not bad, but not quite “returning its yield” either. The stock almost-always shows a high current yield, but its stock price today is 43% below its IPO level – which is where the return slippage is occurring.

Now you could further improve your returns by insisting on only paying 80% of book value or less for PSEC shares. In other words, only paying $0.80 on the dollar for the assets on its books. This strategy would help you time pullbacks almost perfectly, as you’d only have bought in 2008-09, 2011 and 2015-16:

Buy When Price-To-Book (Blue) is Below 0.80

And you wouldn’t buy now. In fact, if you’re looking for high income, don’t reach and buy mREITs or BDCs today. There are better bargains to be had, for secure 7% to 8% yields, with upside to boot.

— Brett Owens

3 Secure Strategies for 8%+ Dividends in 2017 [sponsor]

This year, the best bargains are investment vehicles that have market caps between $1 billion and $3 billion. They’re plenty liquid enough for you and me, but not for the big institutional investors that hold two-thirds of all shares in public stocks.

Combined they make up only a fraction of the stock market’s total capitalization – so they don’t get much coverage from the financial media.

And that makes these ignored corners of the financial markets ideal places for us to search for high yields. Now like any sectors there are good investments and bad investments, of course. So let’s talk about these 3 areas – and how to employ a contrarian approach to find the best values, which I define as secure 8% yields with price stability and even 7% to 15% upside in many cases.

Source: Contrarion Outlook